Beyond Power: The Helium & Tungsten Bottlenecks

The Iran war exposed a wartime logistics shock. China's export controls exposed a structural one.

This analysis is for informational and educational purposes only and does not constitute investment, legal, or financial advice. FPX AI has no positions in any securities mentioned. Do your own research. Geopolitics remain fluid.

The Setup

The market keeps making the same mistake.

It sees a geopolitical shock, finds the scariest input in the stack, and immediately extrapolates to system-wide AI paralysis. This time the input is helium.

That is directionally right and analytically lazy.

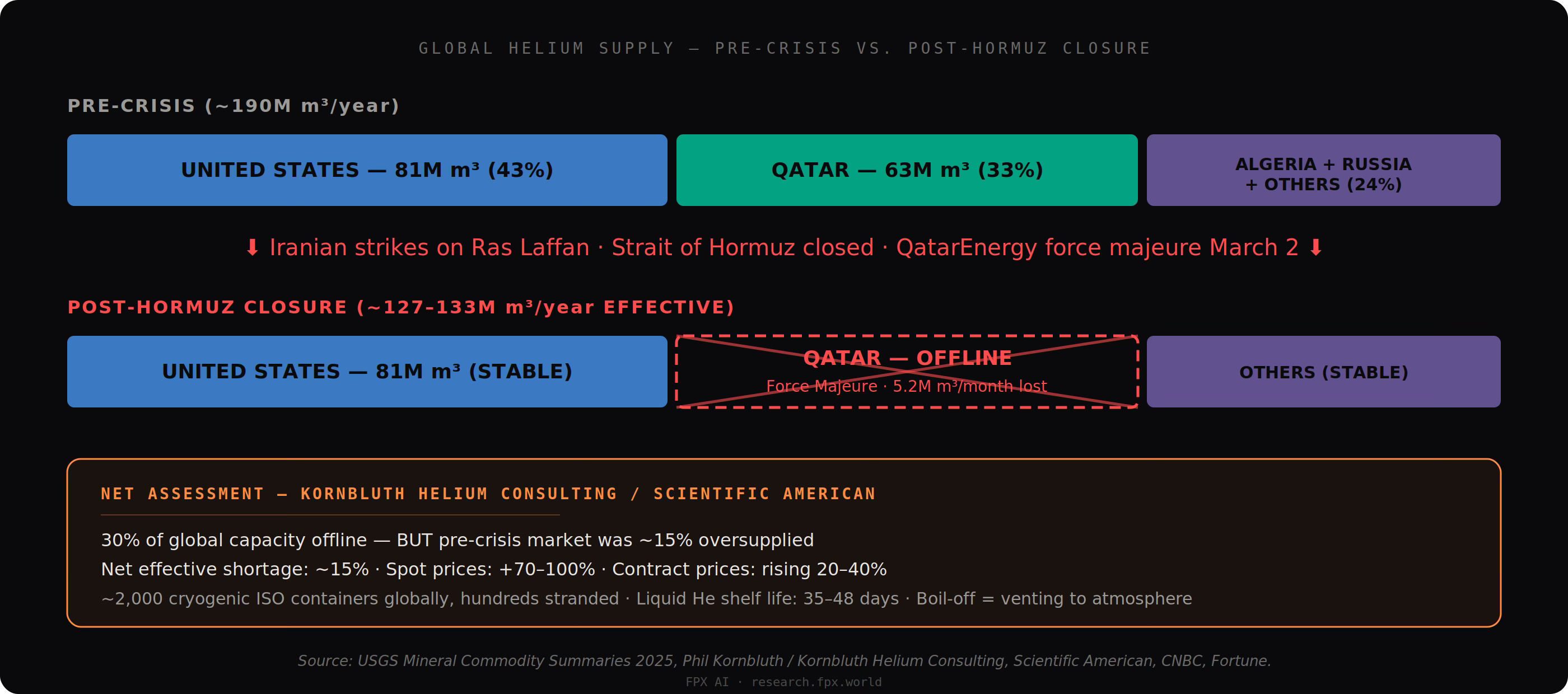

Qatar produced roughly 63 million cubic meters of helium in 2025 out of approximately 190 million globally - about one-third of world supply (USGS Mineral Commodity Summaries 2026). On March 2, 2026, QatarEnergy halted production at Ras Laffan Industrial City - the world’s largest LNG export hub - following Iranian drone and missile strikes. The Strait of Hormuz has been severely restricted, with Iran permitting limited transit only for vessels with no US or Israeli links (Reuters). Qatar’s full helium output went offline immediately; Reuters reports Qatar’s helium output is expected to fall about 14% as a result of the physical damage, though the initial shock removed the full one-third from the market for weeks.

On March 17, Airgas - a subsidiary of Air Liquide (AI.PA) and one of the largest US packaged gas distributors - declared force majeure on helium shipments to US customers, effective 12:01 a.m. Eastern. Letters reviewed by Bloomberg show customer deliveries capped at up to half of normal monthly volumes plus a $13.50 per hundred cubic feet surcharge. Spot helium prices have more than doubled since the conflict began, with some markets reporting surges of 70-100% (CNBC). Hundreds of specialized cryogenic ISO containers, each worth approximately $1 million, are stranded in the Middle East. Helium logistics are time-sensitive: Reuters says liquid helium generally needs to reach end users within about 45 days, so stranded inventory is not a buffer so much as a wasting asset. We are literally losing feedstock to the sky.

This is a real physical-layer shock.

But the market’s next leap is where the analysis breaks. The myth is that a helium disruption automatically means immediate AI infrastructure failure. That is not the right layer. Helium is a real upstream bottleneck in chipmaking and select cryogenic systems. It is not the working fluid of mainstream AI rack liquid cooling - NVIDIA and Schneider both describe modern AI liquid-cooling systems as water- or glycol-based closed loops. The first-order risk is not that every AI cluster suddenly goes dark. The first-order risk is that an already concentrated semiconductor materials chain gets tighter, more expensive, and more selective in who gets priority.

That distinction matters.

Because if you trade this as “AI stops,” you miss the actual structure of the shock. And the actual structure is far more instructive than the headline.

Our house view is straightforward: the supply shock is real. The panic is selective. The market is correct on scarcity and wrong on propagation. The names with weak inventory, weak recycling, and weak procurement leverage should worry. The largest memory players look buffered for now. The risk is duration, not day one. The market is pricing the gross supply loss faster than it is pricing the buffering mechanisms.

That is the setup.

The rest of this piece explains why helium became strategic, where the actual bottlenecks are, which parts of the semiconductor stack are most exposed, why the broad panic is overstated for Samsung (KRX: 005930), SK Hynix (KRX: 000660), TSMC (TSM), and Micron (MU), and which signals will tell you whether this remains a pricing event or turns into a real production event.

As we covered in Parts 1 and 2 of this series - on memory and networking - the market fixates on the components it can see: GPUs, FLOPs, megawatts. The real constraints live in the physical layer surrounding the chip. Helium is as physical as it gets. You cannot synthesize it. For many critical cryogenic and semiconductor uses, substitution is limited or impractical. You can only extract it from the earth, liquefy it at -269 C, and deliver it before it boils away.

Start From Physics, Not Headlines

Helium looks simple. Atomic number two. The second lightest element in the universe. But industrially, it is one of the hardest substances on Earth to handle. Understanding why requires starting from the physics - the foundational principle of every FPX analysis.

Most commodities can be stockpiled, rerouted, blended, or substituted. Helium does not cooperate. It is produced as a byproduct of natural-gas processing. It must be purified to extremely high levels for semiconductor use. It must be liquefied at ultra-low temperatures. It must move in specialized cryogenic containers. And it cannot sit still for long because boil-off destroys inventory value over time. The shock is not just “less helium.” The shock is “less helium in a system that was never built for graceful delay.”

Once you map the full physics of helium supply, one conclusion becomes unavoidable:

Helium is not scarce because it is rare. It is scarce because controlling it sits at the edge of engineering limits.

That is the right starting point.

The Cryogenic Paradox

Most gases cool when you expand them through a valve. This is the basic principle behind every refrigerator - the Joule-Thomson effect. Helium breaks this rule. At standard industrial temperatures, expanding helium through a valve makes it hotter, not colder. To push helium down to its liquefaction point at -269 C - four degrees above absolute zero - you need specialized turboexpander equipment that only a handful of companies manufacture globally. These are not commoditized machines. Lead times for critical liquefaction and purification components can stretch well beyond a year.

The Purity Gauntlet

Semiconductor-grade helium requires ultra-high purity - USGS defines US Grade-A helium as 99.997% or greater, and leading-edge processes use grades up to 99.9999% (six nines). Raw helium extracted from natural gas wells starts at roughly 0.04-0.5% concentration. Getting to semiconductor grade means concentrating the gas over 1,000x and then purifying it through multiple stages spanning a wide temperature range, including high-temperature getter systems that chemically trap impurities down to parts-per-billion. The specialized equipment and materials required for these purification stages come from a small number of suppliers with long lead times.

This is classic FPX territory: the relevant bottleneck is not gross supply. It is qualified supply at the required performance layer. A semiconductor fab does not need generic industrial gas. It needs ultra-high-purity helium delivered reliably into tightly tuned processes. Even if total global supply is only partially impaired, the usable portion for high-performance semiconductor applications can tighten faster than the headline volume loss suggests.

The Storage Problem

Helium is far harder to buffer than most commodities. The SIA says helium cannot be readily stockpiled. Liquid helium constantly absorbs ambient heat. Even in the best cryogenic containers, boil-off runs 0.1-1% per month. Reuters reports that liquid helium generally needs to reach end users within about 45 days. Some underground storage exists - USGS notes cavern storage in Texas - but this is not comparable to a strategic petroleum reserve in scale or accessibility.

And the US no longer has a federal buffer. The Bureau of Land Management completed the sale of the Federal Helium System in June 2024. USGS now lists the government stockpile as none.

This is why hundreds of stranded containers in the Middle East are not a “buffer” - they are a wasting asset evaporating into the atmosphere. For helium, logistics are not a supporting function. They are part of the product. If containers are stranded, helium is not merely delayed. It is physically degrading. This is one of the rare markets where logistics failure becomes literal product destruction.

What Helium Actually Does in a Fab

This is where the most common misunderstanding lives. The popular narrative has framed helium as “the coolant that keeps AI data centers alive.” That is wrong. NVIDIA and Schneider both describe modern AI liquid-cooling systems as water- or glycol-based loops. Helium does not cool your GPU rack.

The right framing: helium is one of the upstream gases that determines whether the chips feeding those data centers can be manufactured without yield loss. It operates at the wafer fabrication layer, not the deployment layer. That is still a serious bottleneck. It is just a different layer of the stack.

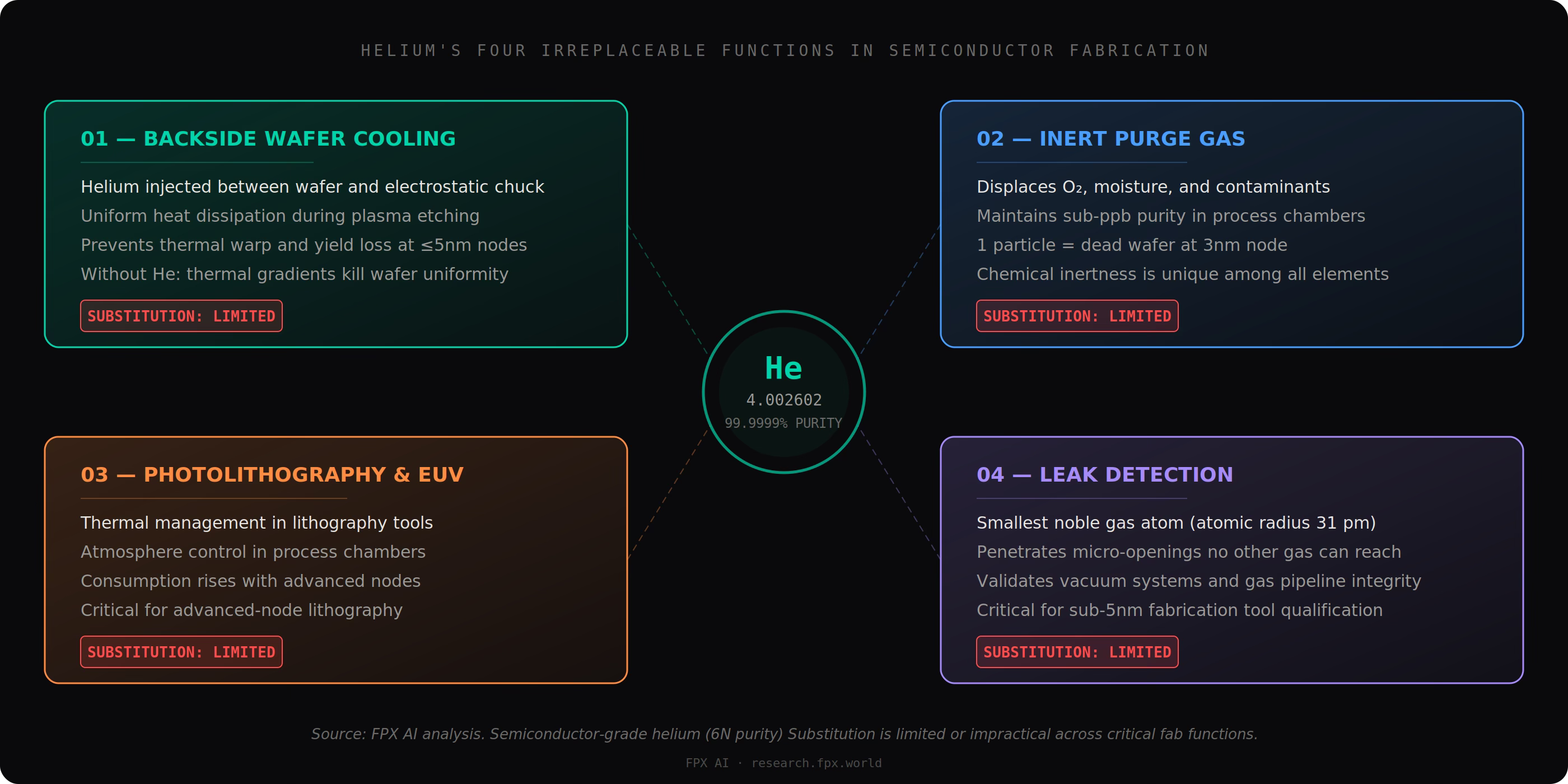

In a modern fab, helium performs four critical functions where substitutes are limited, lower-performance, or hard to qualify:

Backside wafer cooling. During plasma etching, helium is injected between the wafer and the electrostatic chuck to dissipate heat uniformly. Without it, thermal gradients warp the wafer and kill yield at advanced nodes.

Purge gas. Helium’s chemical inertness makes it a primary choice for displacing contaminants in process chambers where a single particle can ruin an entire wafer at 3nm. The SIA notes that many helium uses in semiconductor manufacturing lack viable substitutes.

Photolithography and EUV processes. Helium is used in photolithography environments for thermal management and atmosphere control. The SIA identifies photolithography as one of the critical semiconductor applications for helium.

Leak detection. Helium’s tiny atomic radius allows it to penetrate openings that no other test gas can reach, enabling micro-leak detection in vacuum systems and gas pipelines across the fab.

USGS reports that helium has no substitute in cryogenic applications below -429 F (-257 C). A semiconductor devices professor at South Korea’s Sangmyung University confirmed to TechNews that there is currently no viable alternative for cooling wafers in semiconductor production. The combination of thermal conductivity, chemical inertness, and atomic size is unique among all elements.

USGS reports that controlled atmospheres, fiber optics, and semiconductors together accounted for 17% of US helium sales in 2025. That exposure could rise as advanced-node capacity expands. Helium is embedded in photolithography and other wafer-fab steps, so as fabs push to smaller nodes, fab-level helium exposure can rise. The Semiconductor Industry Association cautioned in 2023 that substantial helium disruption would significantly affect US and global semiconductor manufacturing.

The Supply Chain: Too Few, Too Specialized, Too Slow

The entire global helium supply chain runs through a small number of highly specialized facilities. Lam Research(LRCX) reports that fewer than 20 helium refineries existed globally as of 2021. The exact count depends on whether you are counting refineries, liquefiers, or fully integrated plants. The number is not the point. The point is that the system is too concentrated, too specialized, and too slow to replace on a quarterly timeline.

Pre-crisis, the supply picture looked roughly like this: the United States produced approximately 81 million cubic meters annually (roughly 43% of global output), Qatar produced approximately 63 million cubic meters (roughly 33%), Algeria contributed meaningful volumes, and Russia - which has been expanding production amid its ongoing war in Ukraine - rounds out the top tier (USGS).

Even the more optimistic counterarguments do not dispute the core physics. They dispute whether standalone helium projects - dry-gas plants not tied to LNG infrastructure - can come online faster than the 3-6 years required for LNG-integrated facilities. Even if that is true, it is not useful for an immediate wartime shock.

The Net Shortage Is Not 33%

The critical detail most analysts miss: the pre-crisis helium market was actually oversupplied by roughly 15%. Phil Kornbluth, the most cited independent helium consultant in the world, told Scientific American that with a 30% loss of global capacity offset by a recent 15% supply overhang, the net effective shortage is approximately 15%. Some market observers cited by the Financial Times argue the eventual shortfall could settle closer to 10-15% of demand rather than a full one-third once inventories and alternate supply are factored in.

That is plausible, not settled. But it is the difference between a crisis and a manageable disruption. The deeper point: the market is pricing the gross supply loss faster than it is modeling the buffering mechanisms.

The Logistics Chokepoint

Helium distribution depends on roughly 2,000 specialized cryogenic ISO containers globally (Scientific American). These are not interchangeable with standard LNG or industrial gas containers. Each costs approximately $1 million. Hundreds are now stuck in the Middle East - in Qatar, on cargo ships, or in transit through restricted shipping lanes.

Container transit from the Persian Gulf to South Korea normally takes about one month. Helium that shipped from Qatar before the war started is still arriving. The real shortage at the fab level has not fully hit yet. As Kornbluth told Fortune: the shortage is a few weeks out. It is a sunny day on the beach, but the tsunami is visible on the horizon.

The Timeline: From Ras Laffan to Force Majeure

February 28, 2026. US-Israeli airstrikes on Iran begin. Iran retaliates with drone and missile strikes across the Gulf.

March 2. QatarEnergy halts LNG production at Ras Laffan following Iranian drone strikes on operational facilities. Helium extraction ceases simultaneously. Iran declared the Strait of Hormuz closed to U.S.- and Israeli-linked shipping, severely restricting commercial transit while still allowing limited passage for some neutral vessels.

March 4. QatarEnergy declares force majeure on LNG and associated product contracts, including helium. Approximately 5.2 million cubic meters of monthly helium supply goes offline. Gasworld convenes emergency webinar of industry experts. (C&EN)

March 12. Deutsche Bank notes the market has shifted from oversupplied to undersupplied. Bank of America estimates spot prices have already surged approximately 40%. (CNBC)

March 17. Airgas declares force majeure on helium shipments to US customers, effective 12:01 a.m. Eastern. Letters reviewed by Bloomberg confirm 50% delivery caps and $13.50/Mcf surcharges. Healthcare customers are prioritized over industrial buyers.

March 18-19. Iranian missiles strike Ras Laffan Industrial City directly, causing three fires and wiping out approximately 17% of Qatar’s LNG export capacity. QatarEnergy CEO Saad Al-Kaabi says repairs could take three to five years. (Al Jazeera, Fortune)

March 25-31. Spot helium prices reported at 70-100% above pre-crisis levels. Samsung and SK Hynix shares sell off on headlines. PGMEA prices up 40-50% separately on oil price pass-through. (CNBC, TrendForce)

What the Market Is Getting Right

To be clear, the panic is not fake. The market is right about three things.

The price shock is real. Airgas declaring force majeure and capping deliveries is not a theoretical risk. It is an operating fact. Bloomberg reviewed the letters. The surcharges are live. This is happening now.

The logistics problem is real. If expensive cryogenic containers are stranded and product is boiling off, that is not a sentiment issue. That is a physical loss mechanism. Scientific American reports that the industry relies on roughly 2,000 containers, many of which are now stuck in Qatar or on cargo ships. The initial pinch will feel worse until those tanks are repositioned.

Smaller and less-protected buyers are genuinely exposed. They do not need a global shutdown to get hurt. They only need tighter allocations and higher prices. Reuters reports that some production in the global tech supply chain is already being affected, and prolonged shortages could force slower output or product prioritization.

So this is not a call to dismiss the shock. It is a call to route the shock correctly.

What the Market Is Overstating

The consensus narrative went: Iran war closes Hormuz, helium supply collapses, chip fabs shut down, AI buildout stalls, sell everything.

That narrative is wrong in three specific ways.

Myth 1: “30% of supply vanished, so it’s a 30% shortage”

The pre-crisis helium market was oversupplied. Kornbluth estimates a net shortage of approximately 15%, not 30% (Scientific American). Financial Times reporting suggests the eventual shortfall could settle at 10-15% once inventories and alternate supply are factored in. Significant, but not catastrophic.

Myth 2: “Fabs have one week of inventory”

This was true pre-pandemic. It is no longer true. After the 2022 neon crisis - when Russian supply disruptions threatened EUV lithography gases - every major chipmaker rebuilt safety stocks. Reuters reports that Samsung and SK Hynix hold roughly four to six months of helium inventory. Digitimes confirms South Korean chipmakers have enough to sustain production through at least June. TSMC said it does not anticipate significant impact and maintains multi-source contracts (TrendForce). Micron appears relatively insulated given its US manufacturing footprint. The one-week figure applies to smaller, unhedged fabs - not the companies the market is selling off.

Myth 3: “Helium is the coolant keeping AI data centers alive”

This is the most important correction. Helium does not cool GPU racks. Mainstream AI liquid cooling is water- or glycol-based. Helium operates upstream - at the wafer fabrication layer, not the deployment layer. The right framing: helium determines whether the chips can be manufactured without yield loss. That is a serious bottleneck. It is just a different one than the market is pricing.

The right chain is: Iran war → Hormuz disruption → Qatar helium outage → industrial gas rationing → tighter fab input conditions → selective semiconductor pressure.

Not: Iran war → no helium → AI compute stops tomorrow. That assumption is outdated.

Helium Is the New Neon, but Not in the Way the Market Thinks

The clean historical analogy is neon in 2022.

Back then, the market also jumped from specialty-gas risk to broad semiconductor catastrophe. Ukraine supplied approximately 50% of the world’s semiconductor-grade neon. What actually happened was more nuanced. Shortages were real. Procurement mattered. Inventories mattered. But the strongest operators adapted faster than the headlines implied. No major fab shut down. Production continued.

Helium is arguably worse than neon in one respect: the logistics are even uglier. You cannot store helium indefinitely. You cannot ship it through contested waterways without physical degradation. The boil-off clock runs whether you are at war or not.

But the portfolio logic is similar. You should not ask, “Is helium a problem?” It is. You should ask:

Who is short helium resilience?

That is the investable question.