Delivered Is Not Durable: Why AI Policy Is the Next Infrastructure Bottleneck

Delivered megawatts measure whether capacity exists. Durable megawatts measure whether it can survive the political stack.

1. The next bottleneck

The AI infrastructure conversation has moved through a recognizable sequence of bottlenecks in three years, and each one resolved the same way.

In 2023, the question was chips. Could you get enough H100s, whether the rack would ship, whether your Nvidia allocation would land before your competitor’s. In 2024, the question was power: how many megawatts a site could actually deliver, on what timeline, behind what utility relationship. In 2025, it became cooling and electrical architecture: direct-to-chip versus immersion, 54V versus 800V DC, CDU ownership boundaries.

Each bottleneck resolved into a standard. The standard became a shared map. The shared map became a market. Power did not stop mattering once the industry learned to read a one-line diagram; it became the first question every buyer asked. Cooling did not stop mattering once direct-to-chip entered the shared vocabulary; it became part of the standard capacity screen.

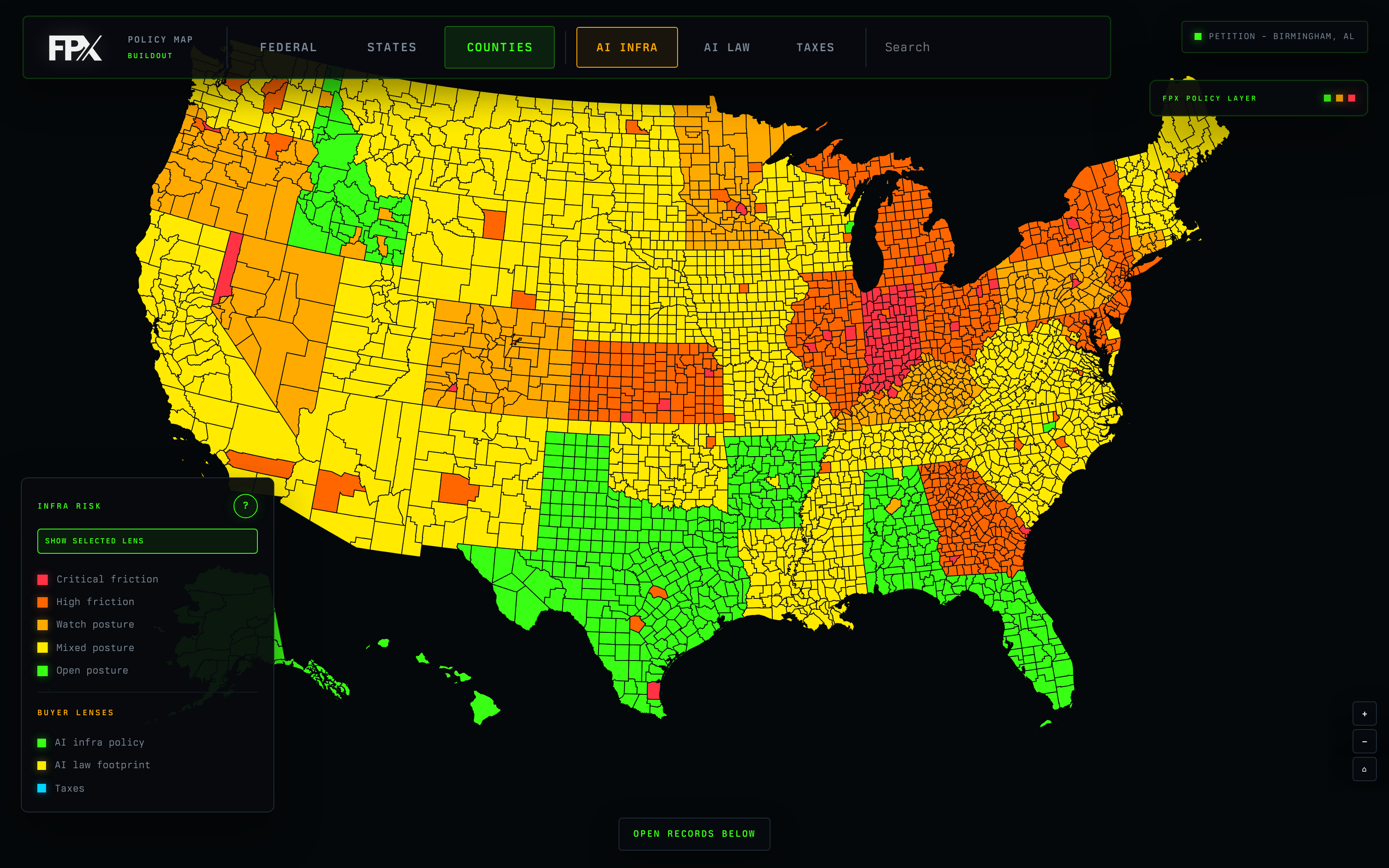

We built a super comprehensive policy map for the AI infrastructure boom. Check it out at policy.fpx.world!!The next bottleneck is in the field but has not been standardized yet. It is not chips, not power, not cooling, not electrical architecture. It is permission: the cumulative political and regulatory consent a project needs to be built, operated, and not reversed.

This is the underlying cause. The transition from AI as product to AI as infrastructure happened in roughly 24 months. In late 2022, AI was a chat interface and an API; buyers were software developers and the unit of work was a prompt. By late 2024, AI was 100MW campuses; buyers were hyperscalers, neoclouds, and sovereign-backed compute companies, and the unit of work was a training run. Once something becomes infrastructure, it becomes politics. Not because anyone decided it should, but because that is what happens when large physical impositions arrive in places where people live.

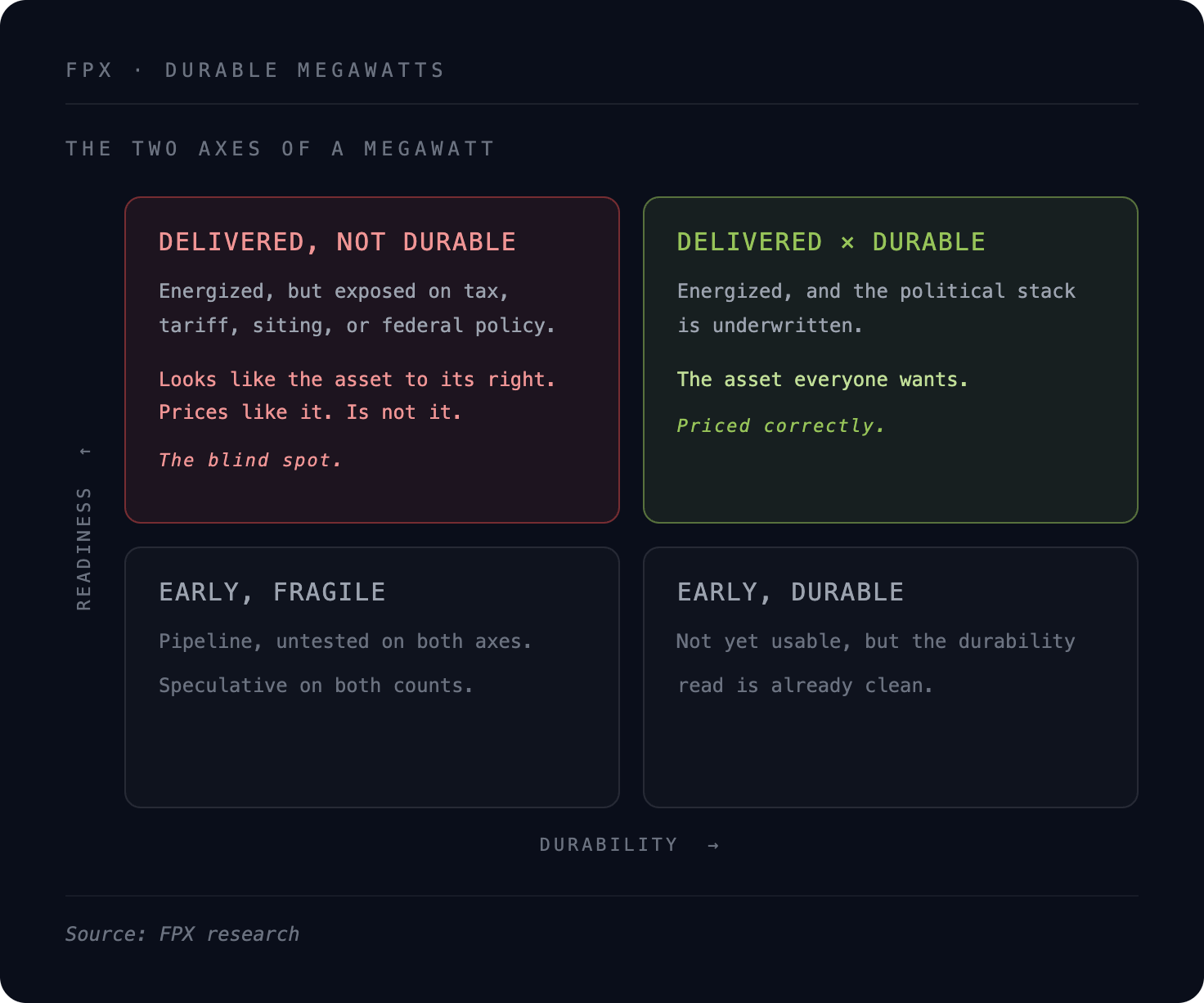

The market has learned to grade capacity on one axis: physical readiness. It now needs a second axis: political durability.

2. Delivered is not durable

A delivered megawatt is energized, cooled, commissioned, contracted, and able to take servers now. That definition closed a real gap in 2024. It separated press releases from operating assets.

But energized is not the same as durable. A megawatt can be delivered against a tax incentive that gets repealed or sunset in the next legislative session. It can be delivered into a county whose political alignment shifts with the next commissioner cycle. It can be delivered under a state regulatory framework that becomes subject to federal challenge, or that survives challenge in a form materially different from the one underwriting assumed. It can be delivered into a market where the utility tariff structure is reopened, or where a moratorium one county over creates a political pattern for its neighbors.

The market already grades megawatts on readiness, and it does it well. The ladder runs announced → optioned → committed → delivered, and each rung strictly contains the one below it.

Announced. Marketing. A press release.

Optioned. Land and early utility positioning. Pipeline risk.

Committed. Real work has started. Studies, permits, equipment strategy, possibly a tenant. Still not usable.

Delivered. Energized, cooled, commissioned, contracted, ready for servers.

That ladder measures one thing: whether the capacity physically exists. Durability is a different question, and it does not sit at the top of that ladder. Durable megawatts are capacity whose political dependencies have been underwritten across the federal, state, and county stack: tax treatment, tariff exposure, siting authority, local opposition, and federal policy exposure. It runs crosswise to readiness. A delivered campus can be fragile. An optioned site can already be durable. The two move independently, and the market prices only one of them.

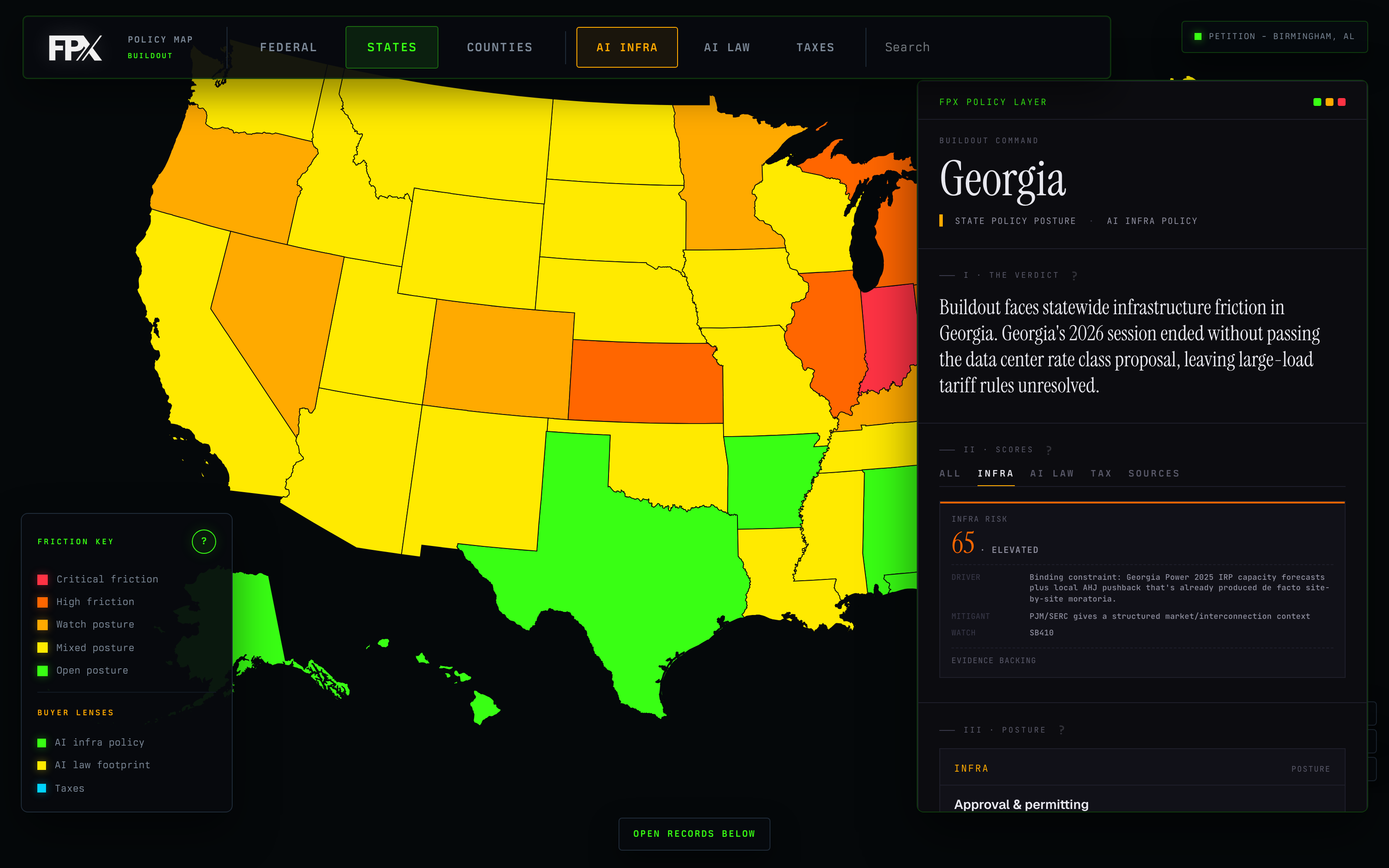

Georgia shows what the second axis looks like in practice. The state offers a high-tech equipment exemption under O.C.G.A. §48-8-3(68.1); exempt purchases by a qualified data-center owner run through December 31, 2031, effectively sunsetting January 1, 2032. The economics of certifying a Georgia campus depend on that program. In the 2026 legislative session, the program drew tax repeal and sunset pressure across SB 408, SB 410, and HB 559. SB 410 passed the Senate on March 6, 2026, then stalled in the House; SB 408 and HB 559 did not reach enactment. Separately, Georgia saw moratorium proposals on data center construction: HB 1012 would have paused construction until March 1, 2027, and HB 1059 would have barred local permits from July 1, 2026 through December 31, 2028. A buyer certifying a Georgia campus in 2027 scored high on readiness and was still exposed: it was underwriting tax durability against repeal proposals and siting durability against moratorium proposals in the same session. None of the bills became law, and the exemption survived the 2026 session intact. The point is not which bill passed. Filed bills are cheap. A session in which tax repeal and moratorium pressure are both moving is a different underwriting environment than one with neither, regardless of outcome. The signal is organized pressure on overlapping timelines, not which bill prevails — and the coalition that produced that pressure can return next session.

The market grades readiness down to the rung. It treats durability, if at all, as a line item called "regulatory risk." Capacity marketed as delivered leads with power, cooling, and delivery date; the political stack rarely arrives as anything a buyer can compare across sites. The public record does not yet give clean spreads between durable and fragile jurisdictions. Political durability gets discussed in diligence, but it does not show up as a standardized adjustment in marketed capacity, RFP comparison, or investor underwriting. The market is not blind to the risk. It lacks a common instrument for grading the second axis the way it grades the first. AI Policy Map is FPX's attempt at that instrument.

3. Why this is the same arc as before

Permission is on the same arc power and cooling followed: first an edge, then a shared language, then table stakes. The advantage is not that political risk remains mysterious forever. The advantage is in defining the schema before it becomes table stakes.

The pattern is older than AI. Electricity went through it in the late 19th century. The Federal-Aid Highway Act of 1956 took years of state-by-state cooperation and rolling local opposition to implement. Cellular towers went through it after the Telecommunications Act of 1996. Each followed a recognizable arc: technical possibility, capital deployment, local resistance, regulatory clarification, eventual normalization. The arc usually takes 15 to 25 years.

AI infrastructure is on the same arc, compressed. The first hyperscaler campuses arrived in the late 2000s. Mainstream awareness arrived in 2023. Active state legislation, federal preemption fights, and organized county-level opposition arrived in 2024 and 2025. What took electricity decades and highways twenty years is taking AI infrastructure five.

The risk profile is also different from prior infrastructure categories. Electricity buildout was driven by utilities operating under a regulated-monopoly framework, where politics affected pace but rarely killed projects. Highway buildout was driven by federal funding with state implementation, where politics affected route but rarely killed the system. AI infrastructure is driven by private capital deploying into a regulatory framework that did not exist five years ago, in counties with no prior data center experience, under state legislatures writing the rules in real time.

The result is a compressed political layer with no historical baseline, applied to an asset class with 5-to-10-year operating lives and 25-year financial structures. That is the underwriting problem. It is not partisan. The relevant variables are: how recent is the data center inflow, how visible are the local impacts, how organized is the citizen response, and how durable is the existing political consensus that brought the investment in the first place.

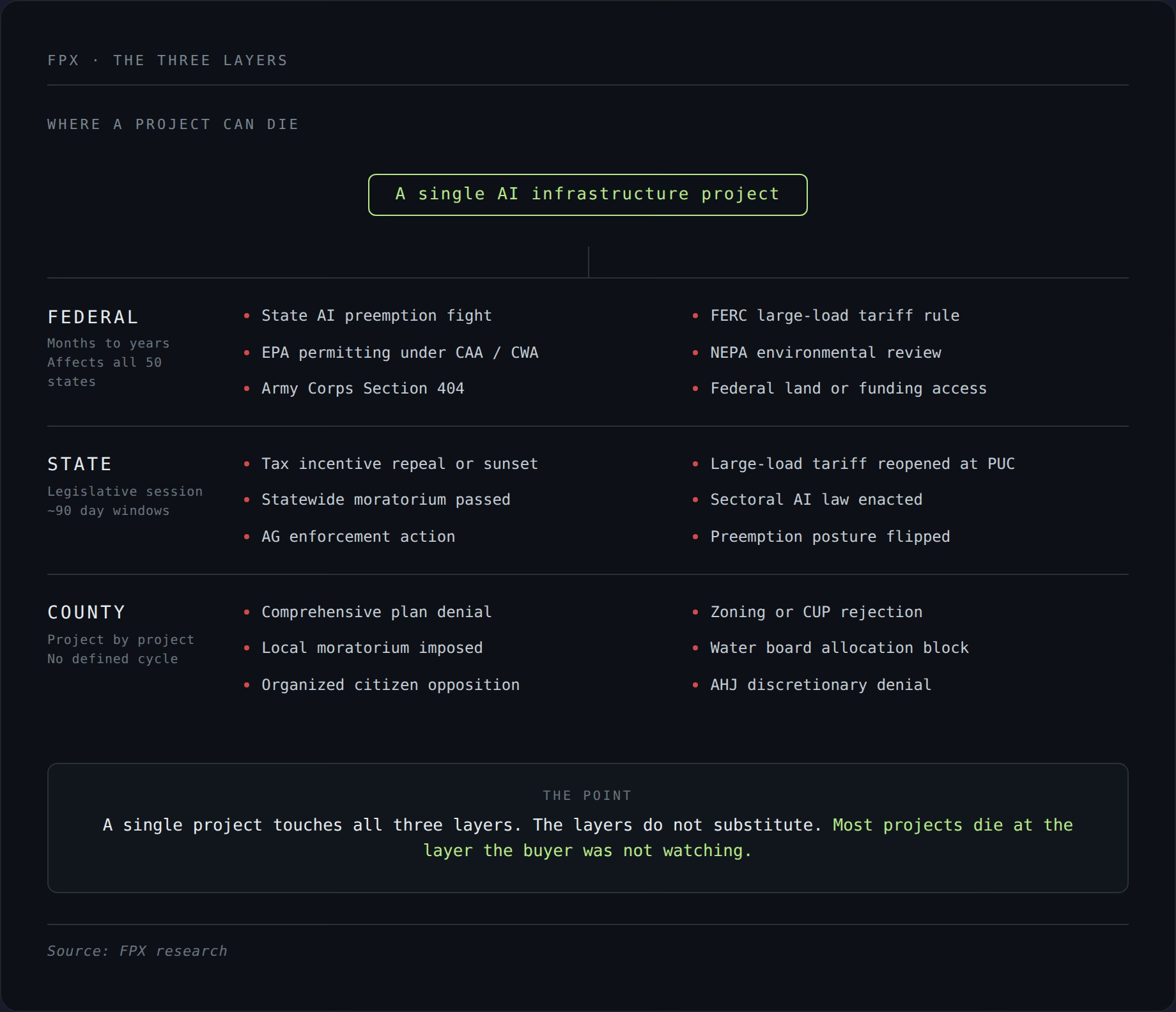

4. The three-layer political stack

Durable megawatts require alignment across three layers, each operating differently.

Federal is the slowest and the highest leverage. The federal government usually does not zone a data center, but it can directly shape whether large AI infrastructure can be permitted, financed, connected, or accelerated. FERC orders on co-located load in PJM reset operating templates. Executive Order 14318 (July 2025) defined qualifying projects at greater than 100MW of AI load and directed agencies toward accelerated review, FAST-41 pathways, and federal land access. Executive Order 14365 (December 2025) created an AI Litigation Task Force focused on state AI laws. In March 2026 the administration published the National Policy Framework for Artificial Intelligence, a legislative recommendation that Congress preempt burdensome state AI laws while preserving state and local zoning authority over AI infrastructure. Federal AI governance and federal data center infrastructure permitting are related but distinct tracks. Federal action is also directionally ambiguous for durability: for an operator exposed to fifty divergent AI governance regimes, federal preemption can be a tailwind; for a project relying on a particular state framework, the same action can be destabilizing.

State is where most operating decisions land. The state controls the tax regime, the legal framework for AI governance, the utility tariff that prices the load, and the preemption posture against local moratoria. A state’s posture can shift meaningfully in a 90-day window. A buyer who treats “the state tax incentive” as a single line item, comparable across 38 states, is operating on a map that does not reflect the territory.

County is where projects actually get built or stopped. The county approves the comprehensive plan, grants or denies the conditional use permit, votes on moratoria, and allocates water draw rights. County action is project-by-project. There is no county policy cycle. The county is also where the available data is thinnest, scattered across roughly 3,143 US counties and county equivalents.

The layers do not substitute for each other. They compound. A state with a durable tax program can still have a county that blocks a project. A county with a permissive zoning history can still be affected by a state legislature that reverses a tax incentive. A state with strong preemption protection can still see its underlying authority challenged by federal action.

The durability stack at a glance

Federal: AI governance preemption · FERC jurisdiction over interstate transmission tariffs, interconnection, and co-located load service · NEPA environmental review · FAST-41 infrastructure coordination · EPA permitting · Army Corps Section 404 · federal land and funding access

State: tax incentives and program durability · repeal, sunset, and amendment pressure · PUC decisions on large-load tariff structure · state-level moratoria and sectoral AI governance · state preemption posture toward local moratoria

County and city: zoning and comprehensive plan land-use designations · conditional or special use permits and site plan review · water and wastewater capacity controlled by the county or local utility · noise, lighting, height, and setback ordinances · local moratoria · organized citizen opposition

5. Field examples: Texas, Georgia, Loudoun

The texture is best seen through specific examples.

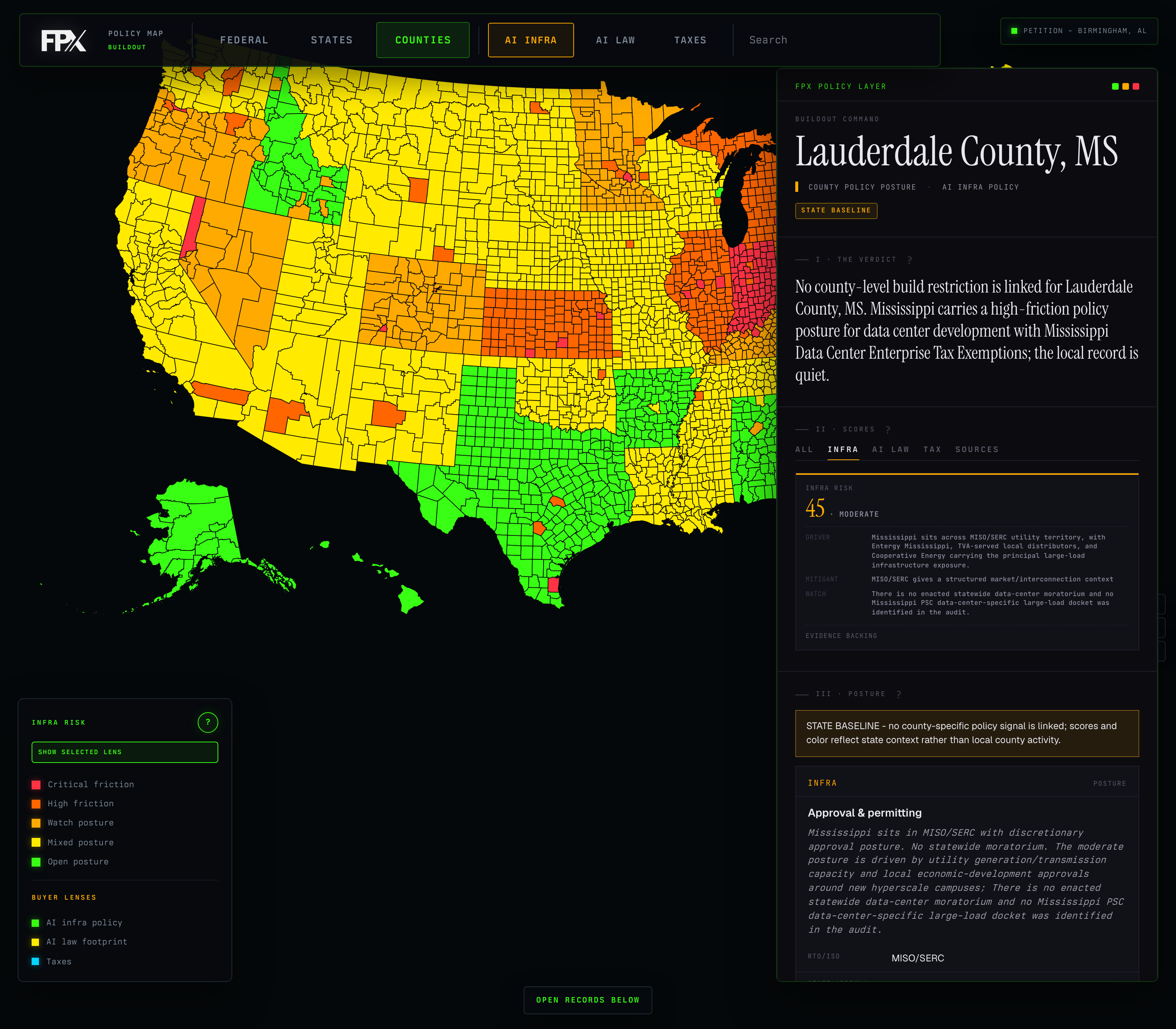

Texas operates two parallel data center tax programs under Tex. Tax Code §151.359 (Qualified Data Center) and §151.3595 (Qualified Large Data Center Project). QDC provides a state sales/use tax exemption with a 10 or 15 year benefit duration. QLDCP provides state and local sales/use tax exemption with a 20-year benefit duration, claimed via Form 01-929. Both programs are politically durable on the tax dimension. But in May 2026, Hill County approved a one-year moratorium on data center construction in unincorporated areas, and a data center developer filed suit against the moratorium later that month. The moratorium does not invalidate state tax certification. It demonstrates that even Texas projects can face county-level delay and litigation. Texas proves that durable state tax does not eliminate county risk.

Georgia is the compounding case. A buyer planning to certify a Georgia campus in 2027 had to underwrite a tax program running through December 31, 2031 against simultaneous repeal pressure (SB 408, SB 410, HB 559) and moratorium pressure (HB 1012, HB 1059). SB 410 passed the Senate; SB 408 and HB 559 did not reach enactment; HB 1012 and HB 1059 also failed. The session closed with the exemption intact. The lesson is not which bill won. It is that tax and siting pressure organized on overlapping timelines in the same session, and the coalition that produced them can return.

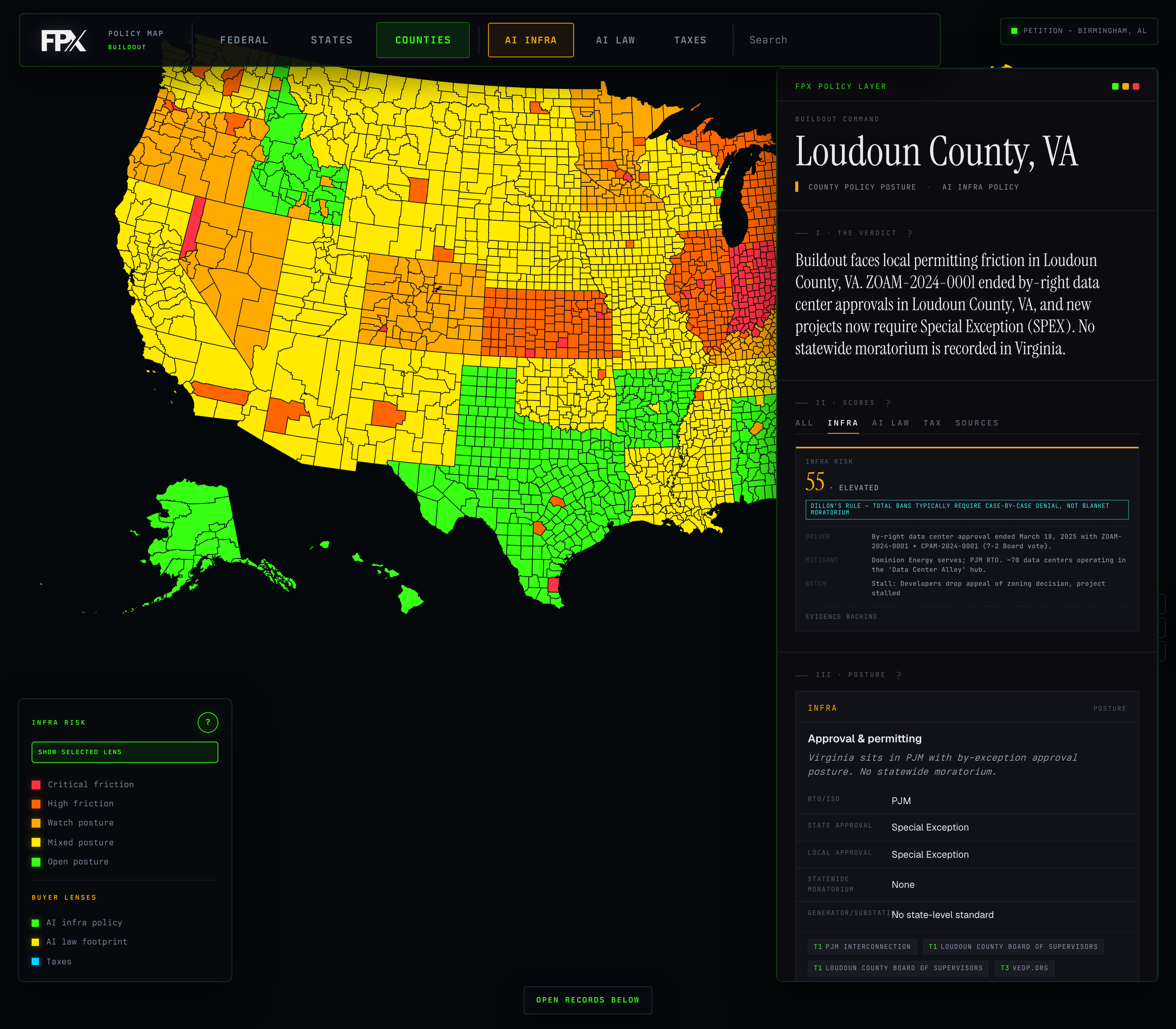

Loudoun County, Virginia presents the opposite pattern. Loudoun is the densest data center cluster in the world, with an installed base measured in gigawatts. The county has been data-center-supportive for fifteen years. But organized citizen opposition has formed around comprehensive plan revisions touching data center zoning, noise ordinances, and transmission line routing. Loudoun’s Phase 1 revisions moved data centers to conditional or special exception (SPEX) uses in zones where they were previously by-right. A buyer underwriting Loudoun in 2026 is operating in a politically shifting jurisdiction, even though the state-level posture remains supportive. Loudoun proves that even mature clusters can become politically unstable.

Each example shows the same structural pattern: a project that looks underwritten on the physical layer carries political exposure that is not visible from the power, land, fiber, and tariff variables the market traditionally diligences. Each of these jurisdictions has a live read on AI Policy Map.

6. Why the market lacks a shared map

The political layer is not invisible. Sophisticated sponsors already diligence it through government-affairs teams, local land-use counsel, utility lawyers, site-selection consultants, and county relationships. That work is real. It produces site-specific opinions for site-specific decisions.

The gap is that this work does not normalize. A government-affairs read on Loudoun does not become a comparable artifact alongside a government-affairs read on Hill County. Each project rebuilds its own diligence. Each buyer carries the cost of bespoke work that the market could in principle share.

Federal data is public but fragmented. State data is fragmented across 50 jurisdictions; NCSL maintains useful trackers showing 38 states with dedicated data center tax incentives, proposals to amend in at least 28 of them, and 14 states considering bans or moratoria, but these are periodic snapshots that do not capture day-to-day durability. County data is the thinnest layer by a wide margin, scattered across PDF meeting minutes, local newspaper archives, board of supervisors agendas formatted differently in every jurisdiction, and comprehensive plan revisions on planning department websites.

The shape of available information runs inverse to the shape of operational risk. Federal posture is easier to read than state posture. State posture is easier to read than county posture.

The first organizations to build a shared, refreshed, source-backed schema for this stack will shape the category before it becomes table stakes.

7. What new diligence looks like

The political stack is now part of the capacity stack. The questions are different for each side of the table.

For operators. The product is no longer the hall, and no longer just delivered megawatts. It is delivered megawatts with documented political durability: federal exposure of the host state, legislative posture in the current session, tax program statute and certification cutoff, local AHJ baseline and any active citizen organization, comprehensive plan posture, recent ordinance history. Treat the political layer as a sales artifact, not as a risk to manage.

For buyers. Before underwriting a site on power and tariff, read the federal layer for whether the host state is in active preemption challenge and whether that challenge stabilizes or destabilizes. Read the state layer for tax durability, repeal and sunset pressure, legal regime, and preemption posture. Read the county layer for active opposition, recent ordinance changes, AHJ discretion, and political memory. This is not legal diligence. It is operating diligence. The diligence is asymmetric across project sizes: a 2MW inference deployment carries primarily state-level governance exposure; a 100MW training campus on a greenfield site carries the full three-layer stack. The cheapest power in a fragile county is not cheap. The strongest tax abatement in a state with active repeal pressure is not strong.

For neoclouds. The political exposure per dollar deployed is structurally higher than for hyperscalers, because the underwriting framework is the same but the balance sheet to absorb mistakes is not. A hyperscaler that mis-prices political risk on a 200MW campus has counterbalancing assets and a multi-year planning horizon. A neocloud that mis-prices political risk on a single 20MW deployment is exposed to the full impact on the next equity round, the next debt facility, the next tenant contract. The cost of getting it wrong shows up as a quiet erosion of operating margin when a tax certification gets re-scoped, a tariff structure gets reopened, or a local moratorium delays a planned expansion. For 5-to-50MW deployments, the state layer usually carries the highest leverage, but county signals still determine expansion risk.

For investors. Underwrite this like infrastructure, not like real estate. A data center asset whose returns depend on a state tax program with active repeal or sunset pressure is not a stable infrastructure asset. It is a leveraged position on legislative outcome. The discount belongs to assets that look cheap on a static read but carry political exposure that compounds over the underwriting horizon. The market is not yet underwriting this discount in a consistent, comparable form. Underwrite the part of the stack the market has not yet standardized.

8. Buildout Command methodology

Naming the bottleneck is easier than measuring it. The schema treats policy as an operating input, not a stream of headlines.

The unit of analysis is the policy fight, not the individual bill. A state legislature may have a dozen active bills touching data centers in a single session, but those bills often belong to a smaller number of underlying conflicts: tax exemption durability, moratorium authority, large-load tariff treatment, local preemption, water disclosure, or sectoral AI governance. Bills are artifacts. The fight is the analytical object.

The federal layer is organized by actor. The White House directs, executive agencies implement, independent agencies regulate, courts adjudicate, and Congress codifies, blocks, or reframes. Reading the federal layer means identifying which actor is moving the relevant question.

Direct evidence is distinguished from inherited baseline. Every jurisdiction gets a structured read, but the system separates local evidence, state rolldown, and baseline-only coverage. A county with no recorded local activity is not the same as a county with active opposition. Where direct evidence is absent, the system says so explicitly rather than filling the gap with synthetic confidence.

Tax programs are modeled at the rule level. A data center incentive is rarely a simple yes/no field. Eligibility can depend on county population, capital expenditure, job creation, tenant versus operator role, electricity treatment, construction purchases, certification timing, reporting obligations, clawbacks, and sunset dates. Kentucky's expanded incentive is the clean illustration: it is not one rule but a ruleset with different minimum investment thresholds keyed to county population. Collapsing that into "tax incentive: yes" loses the information that actually matters commercially.

Three lenses, one evidence base. The infrastructure lens asks whether a campus can be permitted, powered, and locally approved. The tax lens asks whether incentives are usable, durable, and commercially relevant. The governance lens asks whether AI-specific law, federal preemption, enforcement, or disclosure regimes create exposure.

The schema is event-driven, not periodic. The failure mode of every public tracker is that it refreshes on a calendar, so it captures a session months after the session moved. Here the unit that updates is the fight, and the triggers are events: a bill changes status, an agency files, a county posts an agenda or votes an ordinance, a utility opens or closes a docket, a court issues a ruling. Each event updates the affected fight's phase, momentum, and direction, and stamps the jurisdiction read with a new timestamp and source. The operating question a user asks is never "what color is this county?" It is "what do we know, how recently, and what would change the conclusion?" A read carries its own freshness: when it was last touched, what source touched it, and how confident that source is. A jurisdiction that has not been checked since the prior session is marked as such rather than presented as current. That is the difference between a living schema and a snapshot with nicer packaging.

Provenance is tiered. Primary statutory, agency, utility, court, and official local records are distinguished from aggregators, trade coverage, and news signals. Discovery signals are useful but not equivalent to verified legal or administrative facts.

9. The FPX view

The AI infrastructure market is not in a bubble, and it is not blind to political risk. The sophisticated end of the market already diligences it. The sort has now moved past the physical layer.

Two years ago, the question was whether a site had power. Eighteen months ago, the question was whether a site had delivered, commissioned, cooled power. Today the question is whether a site has politically durable power.

FPX has started building the shared schema this essay describes. The map lets users toggle federal, state, and county layers, then read each through infrastructure, tax, or governance lenses, with live records below the map and jurisdiction dossiers on click. The current product should be read as a policy-friction and evidence-coverage map. It is not a legal opinion, a tax opinion, a utility interconnection study, or a permit guarantee.

A misjudged power study can be redesigned. A misjudged political stack can take down a 100MW commitment with no clean recovery path.

That is the game now. The winners will be the ones who read the stack before it becomes table stakes. Read it at policy.fpx.world.

Sources

Federal: EO 14318, data center permitting (July 2025) · EO 14365, national AI policy framework (December 2025) · National Policy Framework for Artificial Intelligence (March 2026) · FERC PJM co-located load action · National Interstate and Defense Highways Act (1956)

State and program: NCSL data center tax incentive tracker · NCSL data center moratorium tracker · Texas Comptroller data center exemption guidance · Georgia DOR Rule 560-12-2-.117 · LegiScan SB 410 · Inside Climate News on Georgia 2026 session · Kentucky HB 775 / Stites summary

Local: NACo data center primer · NACo, What Are Counties? · Loudoun County Data Center Standards & Locations · KWTX on Hill County moratorium and developer lawsuit

This essay synthesizes public sources as of the publication date. Bill numbers, statuses, and program details change on legislative timelines; readers underwriting specific projects should verify current status against the underlying source.

https://shapeofcinema.substack.com/p/im-with-stoopid?r=8dbojf&utm_medium=ios