The World’s Fastest AI Chip Has a Real-Estate Problem

Cerebras just committed 750 megawatts to OpenAI and landed inside AWS. The hard part is not the silicon. It is finding buildings that can actually host it.

Cerebras serves some of the fastest publicly measured inference in the market.

That claim now survives contact with independent testing. On several models available through its cloud, Cerebras sits at or near the top of the output-speed tables, often by a wide margin. OpenAI has committed to 750 megawatts of Cerebras capacity. Cerebras has announced that AWS is putting CS-3 systems inside AWS data centers and plans to expose them through Bedrock.

This is no longer a science project. It is an infrastructure ramp at the scale of a small power utility.

That crossing, from selling a fast chip to operating gigawatts, moves the question that matters. For the models visible in public benchmarks, speed is no longer the open question. What is not settled is whether this hardware can be powered, cooled, sited, and financed at scale, and what that costs the people who have to host it.

There is a popular shorthand for the hard part: that a chip this hot must need exotic, near-freezing water and chillers running around the clock. The reality is narrower, and more interesting. The constraint is not a deep-freeze. It is a particular cooling envelope, cooler water and far higher flow than a GPU rack, landing in a market that is standardizing around the opposite.

That is our subject.

One conclusion is worth stating before the plumbing. “GB200-ready” and “CS-3-ready” are different physical products, and the market does not yet price them separately. The older chilled-water campuses the GPU market has written off may be the fastest wafer-ready megawatts in inventory, and some of the new warm-water halls it prizes are the wrong buildings for this tenant entirely. That mispricing is the thesis. The rest of this report is the evidence.

Where We Pick Up

The silicon has already been covered well. Independent teardowns, SemiAnalysis’s chief among them, have gone deep on the architecture, the bill of materials, the on-chip memory constraint, the off-wafer bandwidth problem, and the workloads where the wafer wins. We are not going to re-litigate any of that.

A silicon teardown cannot answer the questions an operator actually has.

What does the CS-3 facility envelope cost per megawatt once climate and plant design are included.

Which data halls can host it without rebuilding the cooling chain.

And where does a 750 MW committed ramp, with an option path to 2 GW, physically land.

That is the gap. And that gap is our entire business.

So this report checks the public engineering claims against Cerebras’s own CS-3 specifications, separates equipment requirements from site-specific design choices, and then adds the OpenAI contract, the AWS deployment, public colocation agreements, and the economics of cooling.

One note before we start. Published specifications are treated as specifications. Company claims are labeled as company claims. Every dollar figure marked as an FPX scenario is a planning calculation, not a measured PUE, an audited result, or a vendor quote.

Part I: The Chip, the Box, and a Business That Changed Shape

A Chip the Size of a Dinner Plate

Most chipmakers take a 300 mm wafer and cut it into hundreds of processors. Cerebras turns nearly the whole wafer into one processor.

The current Wafer-Scale Engine, WSE-3, is built on TSMC’s 5 nm process. Cerebras publishes four trillion transistors, 900,000 AI cores, 44 GB of on-chip SRAM, 21 petabytes per second of memory bandwidth, and 1.2 terabits per second of external I/O for the CS-3 system.

The memory bandwidth is the center of the thesis.

Decode repeatedly pulls model weights into compute to generate one token after another. A GPU does that from HBM. Cerebras keeps the active weight shard in SRAM on the wafer, close to the cores, and pipelines activations between wafers when a model is too large for one 44 GB device.

That last point matters. “The whole model lives on one chip” is a clean marketing simplification, not a universal description of large-model serving. The more precise claim is still powerful: each shard can remain in on-chip SRAM during decode, reducing the weight movement that constrains conventional accelerators.

The trade-offs are just as physical.

Forty-four gigabytes is enormous for SRAM and small beside the HBM capacity of a modern GPU rack. Off-wafer bandwidth is limited relative to the amount of compute on the wafer. And the engine runs hot: Cerebras’s published specifications put maximum system power at 27 kW, and public technical write-ups have cited figures from roughly 23 to 27 kW depending on configuration.

Cerebras is not trying to be the right tool for every workload. Its sharpest advantage is where low-latency decode and extreme memory bandwidth matter enough to justify a specialized system. That is narrower than “replace the GPU.” It is also a large market.

The Box, and the Number That Actually Matters

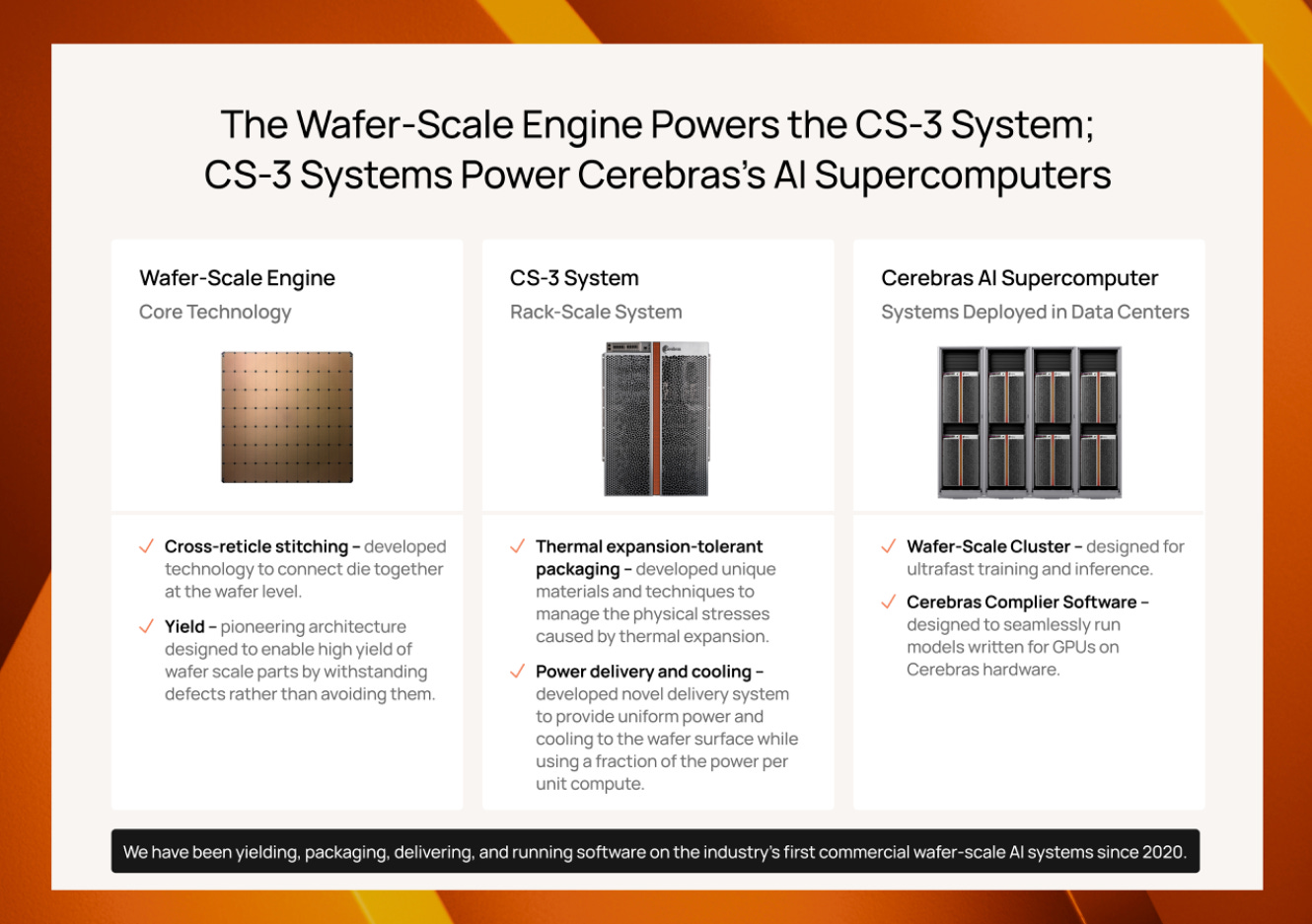

The wafer ships inside the CS-3, a 16-RU liquid-cooled chassis, roughly the size of a small refrigerator.

Forget the silicon for a moment and look at the box from the loading dock. What an investor underwriting a site, or an operator quoting capacity, needs is not the transistor count. It is the short list of numbers that decide which buildings can physically accept the machine and what the cooling will cost to run. Cerebras publishes five that matter:

27 kW maximum system power.

100 LPM of liquid flow per system.

20 ± 2°C water at the system.

Two CS-3 systems and 54 kW total power per rack.

50.4 kW of rack heat rejected to water and 3.6 kW still rejected to air.

The CS-3 is therefore not a 130 kW GPU rack in a different costume. It is a roughly 54 kW WSE rack with an unusually high coolant appetite per kilowatt. Cerebras’s published cluster configurations also add network cabinets, so the full facility model must use the provisioned cluster rather than multiplying WSE racks alone. SemiAnalysis’s teardown adds another line to that bill: each CS system pairs with a separate KV-cache offload node, a dual-socket CPU box carrying six terabytes of DDR5.

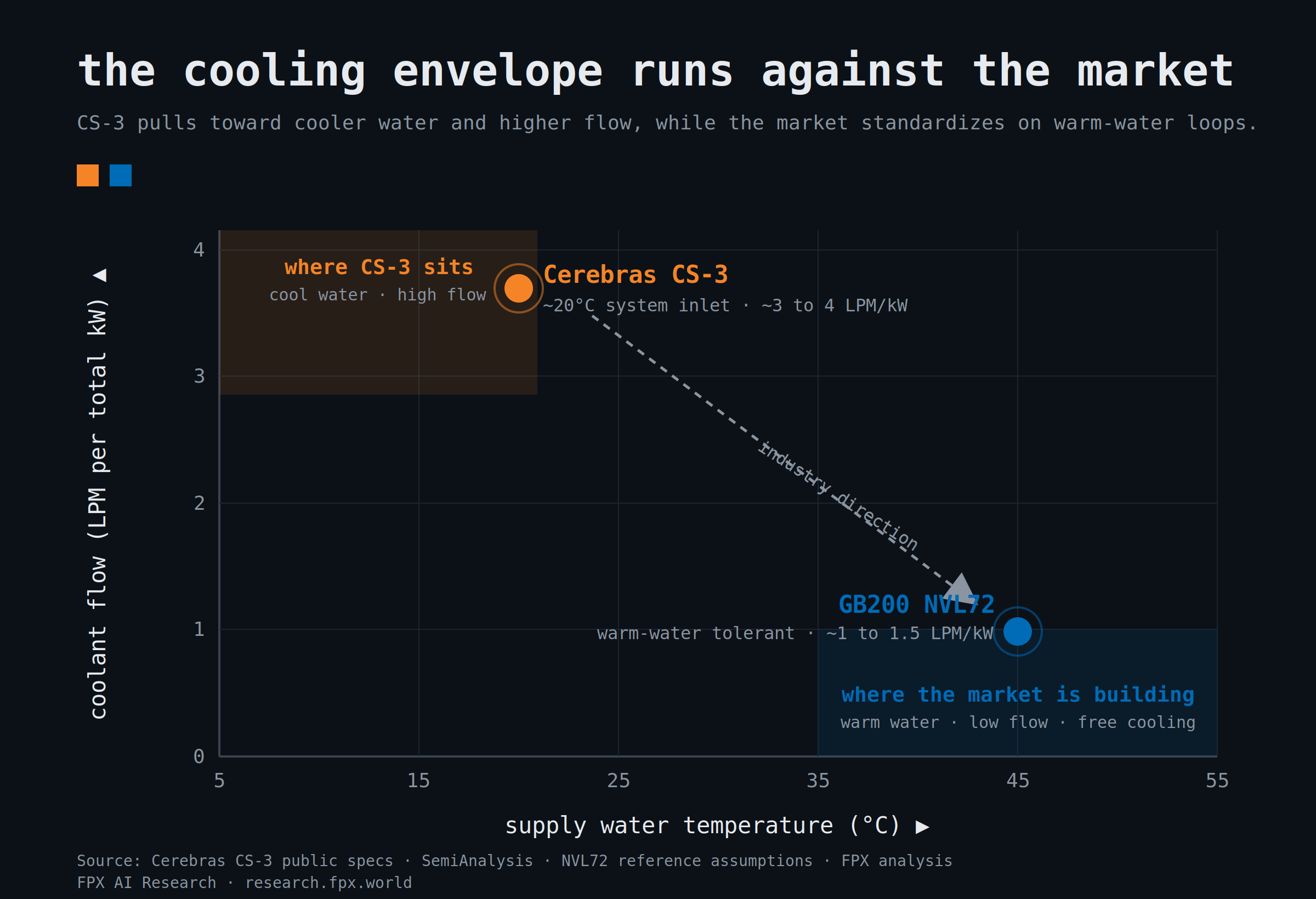

Normalize those numbers on the water side, the same basis for both machines. At maximum power the CS-3 moves 100 LPM against roughly 25.2 kW of liquid heat, about 4.0 liters per minute for every kilowatt it rejects to water. A representative GB200 NVL72 implementation from QCT specifies up to 130 LPM for 115 kW of liquid heat removal, about 1.1 LPM per kW, and supports liquid inlet temperatures up to 45°C. Measured against total system power instead, the CS-3 figure is 3.7 LPM per kW; either basis tells the same story, but the water-side comparison is the like-for-like one.

The exact Blackwell number varies by OEM and design point. The direction does not. CS-3 asks for materially more flow per kilowatt and materially cooler water at the equipment boundary.

The flow tells you something else.

At 100 LPM and roughly 25.2 kW of water-side heat per CS-3, the implied coolant temperature rise is only about four degrees Celsius, using a water-like heat capacity as a planning approximation. That narrow delta-T is why flow becomes a facility issue. The operator has to move a lot of liquid to carry each kilowatt away without letting the coolant warm very much. The Blackwell comparison makes the point: QCT’s design accepts a wide rise, from a 45°C inlet to a 65°C return, so it can move far less water per kilowatt.

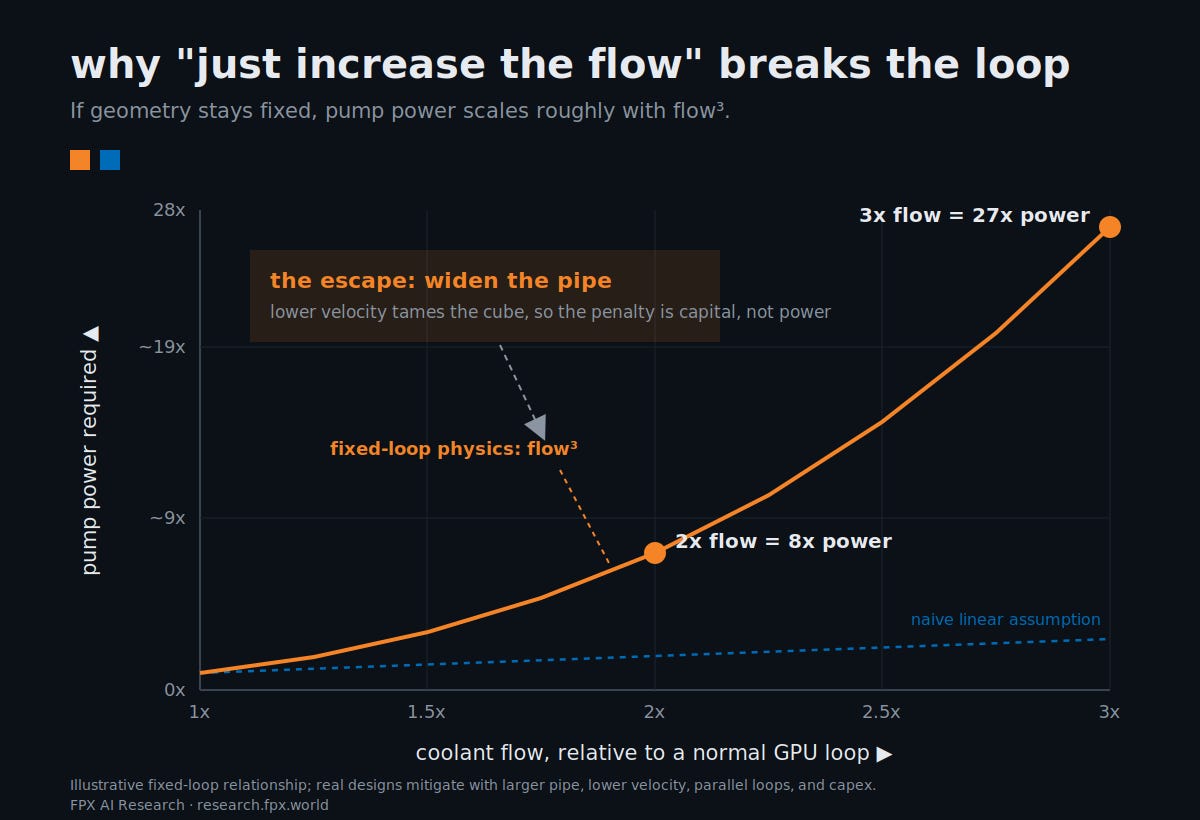

That high flow is also why a CS-3 hall cannot be conjured by turning up the pump on an existing loop. Pump power scales with roughly the cube of the flow rate (P ∝ Q³). Push two to three times the volumetric flow through pipes sized for a normal GPU loop and pump power climbs not by two or three times but by roughly an order of magnitude or more, the cube of two being eight and the cube of three twenty-seven, and the loop runs out of pressure margin long before it gets there. So you do not turn up the pump. You widen the pipe, which drops the velocity back down and tames the cube. That is the trade the operator is actually making, and it is a capital trade: larger headers, pumps, CDUs, valves, manifolds, and quick-disconnects, bought once, to avoid a ruinous recurring power bill.

That is the nuance to hold onto. The penalty here is mostly capital, not operating. Once the loop is correctly sized, steady-state pump energy does not rise three-for-one with flow; it depends on pressure drop, pipe sizing, control strategy, and efficiency, all of which a competent design flattens. Anyone pricing this from raw flow alone, in either direction, is pretending to know the hydraulic design.

The 5°C Number, Correctly Understood

The machine spec, 20 ± 2°C at the machine, tells you what the CS-3 wants. It does not tell you what the building behind it has to do to deliver that. There is essentially one public data point on the building side, which is why it gets repeated so often: a single, much colder number, 5°C.

Here is where it comes from. Cerebras runs much of its fleet itself, and its flagship self-operated site is a 10 MW facility in Oklahoma City, built with Scale Datacenters. SemiAnalysis’s reporting on that site describes a 6,000-ton plant producing 5°C primary water, warmed through a heat exchanger before it reaches the CS-3 at about 21°C.

That is useful evidence about one building. It is not a universal 5°C machine requirement.

Cerebras’s own description of that site adds the other half of the picture: its closed-loop cooling relies on outside air except on the hottest days. Together, the 20°C machine spec and that free-cooling claim rule out the bluntest version of the “compressors run year-round” thesis.

A chilled-water plant can include water-side economization. In cool weather, towers or dry coolers can reject heat without running the chiller compressors, even while the building maintains a chilled-water architecture. The warmer the required supply temperature, the more hours that strategy can work. The colder the required supply temperature, the fewer hours it can work.

So the honest claim is narrower.

A 20°C equipment inlet generally offers fewer economizer hours and less design margin than a 35°C-to-45°C warm-water loop. The penalty depends on local wet-bulb and dry-bulb conditions, approach temperatures, redundancy, heat-exchanger design, and whether the site uses evaporative, dry, or hybrid heat rejection.

There is no universal Cerebras PUE hiding in a spec sheet.

There is a site model.

From Chip Company to Capacity Integrator

Two agreements changed the shape of the business.

The first is OpenAI.

OpenAI has committed to 750 MW of Cerebras capacity, delivered in three 250 MW increments by the ends of 2026, 2027, and 2028. The filed master agreement gives OpenAI options for additional capacity: the Q1 2026 10-Q puts the option at a further 1.25 GW in tranches by the end of 2030, to 2.0 GW in total. Initial press reports valued the committed deal at more than $10 billion; disclosures around the S-1 and first-quarter results describe the master agreement as worth more than $20 billion, and the company carried $25 billion of remaining performance obligations at March 31, 2026.

The contract structure matters as much as the megawatts.

The agreement allows Cerebras to use data centers controlled by Cerebras, OpenAI, or third-party subcontractors, and makes Cerebras responsible for any subcontractors it engages. OpenAI is responsible for the pass-through expenses, and Cerebras’s financial disclosures describe those as customer-specific data-center costs carried at fixed, minimal gross margins.

The working-capital point is not hypothetical, and the filings put a price on it. OpenAI funded a $1.0 billion secured loan to Cerebras in January 2026, restricted to the MRA buildout, bearing 6% interest unless waived or deemed paid under the agreement, repayable in cash or through delivered capacity and services; by March 31, $21.7 million had already been worked off as non-cash billings. If the MRA terminates for reasons other than OpenAI’s uncured breach, the note can accelerate. The customer is financing the buildout it is buying, which is the clearest public evidence that the binding constraint on this ramp is capital reaching service, not silicon.

In plain terms, Cerebras is becoming a capacity integrator. It can lease the building, install and operate the specialized compute, and pass much of the facility bill to OpenAI.

That distinction matters for the thesis. Higher facility cost does not necessarily hit Cerebras as a dollar-for-dollar gross-margin loss under this contract. It hits the customer’s all-in cost, the number of sites that qualify, the working capital required to reach service, and the risk of missing a capacity deadline.

The second agreement is AWS.

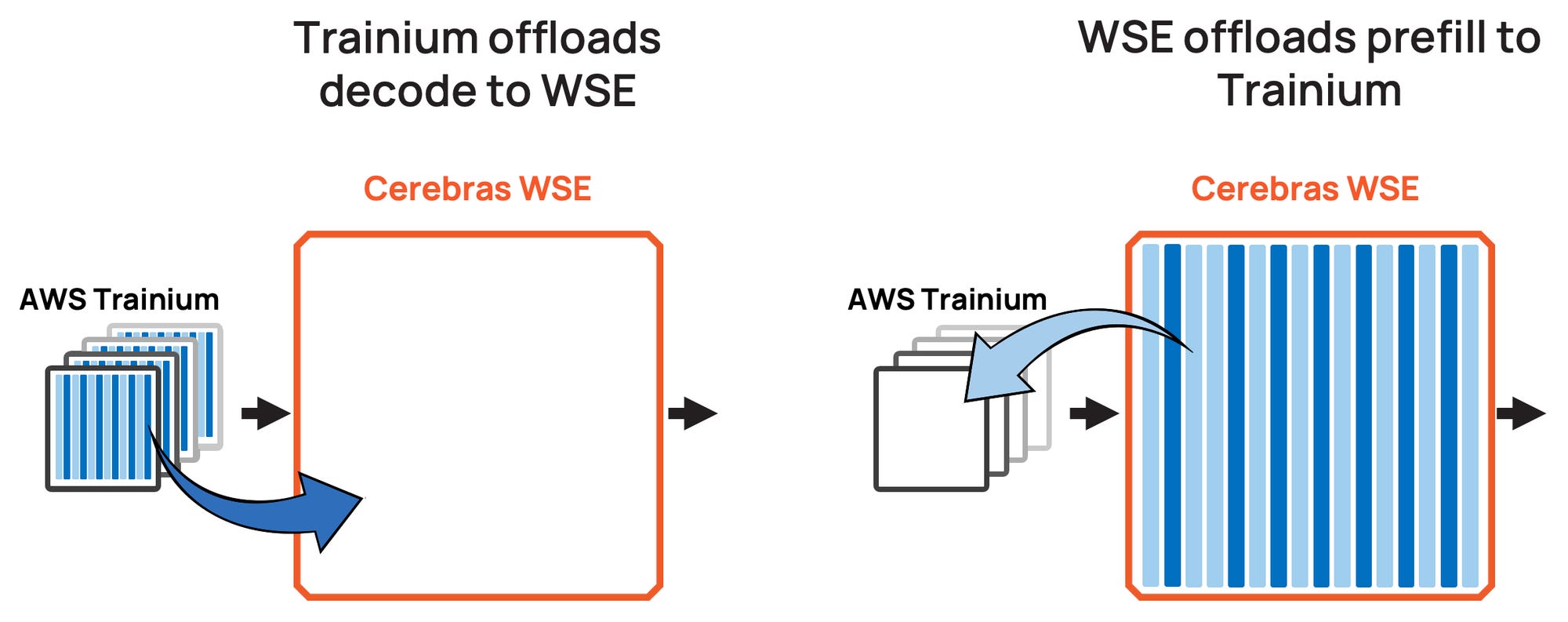

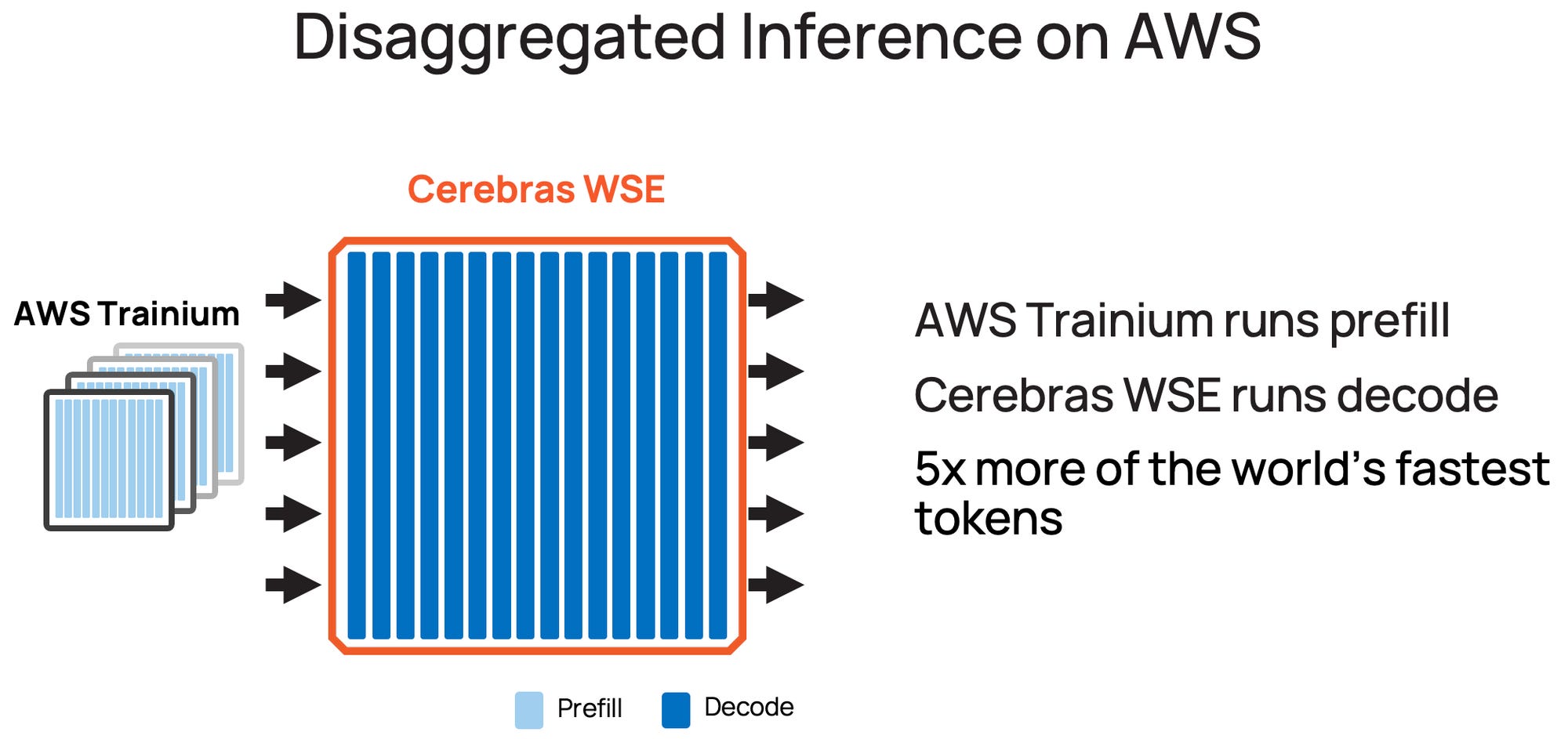

Cerebras says AWS is deploying CS-3 systems inside AWS data centers for a Bedrock service. The companies are also developing a disaggregated design in which Trainium handles prefill and Cerebras handles decode over Elastic Fabric Adapter. Cerebras claims the configuration can deliver five times more high-speed token capacity in the same hardware footprint.

That five-times figure is a vendor claim, not an independent measurement. The facility signal is still strong.

AWS is willing to absorb the integration work inside its own estate. That validates the system’s commercial relevance. It does not prove that an ordinary warm-water colo hall is ready for the same deployment.

If you are AWS, Scale Datacenters, or another operator working directly with Cerebras, the CS-3 can be engineered into the building.

If you are not, it is not a normal tenant move-in. It is a project.

Part II: Three Questions a Chip Analyst Never Has to Ask

Question One: What Does the Facility Envelope Cost Per Megawatt?

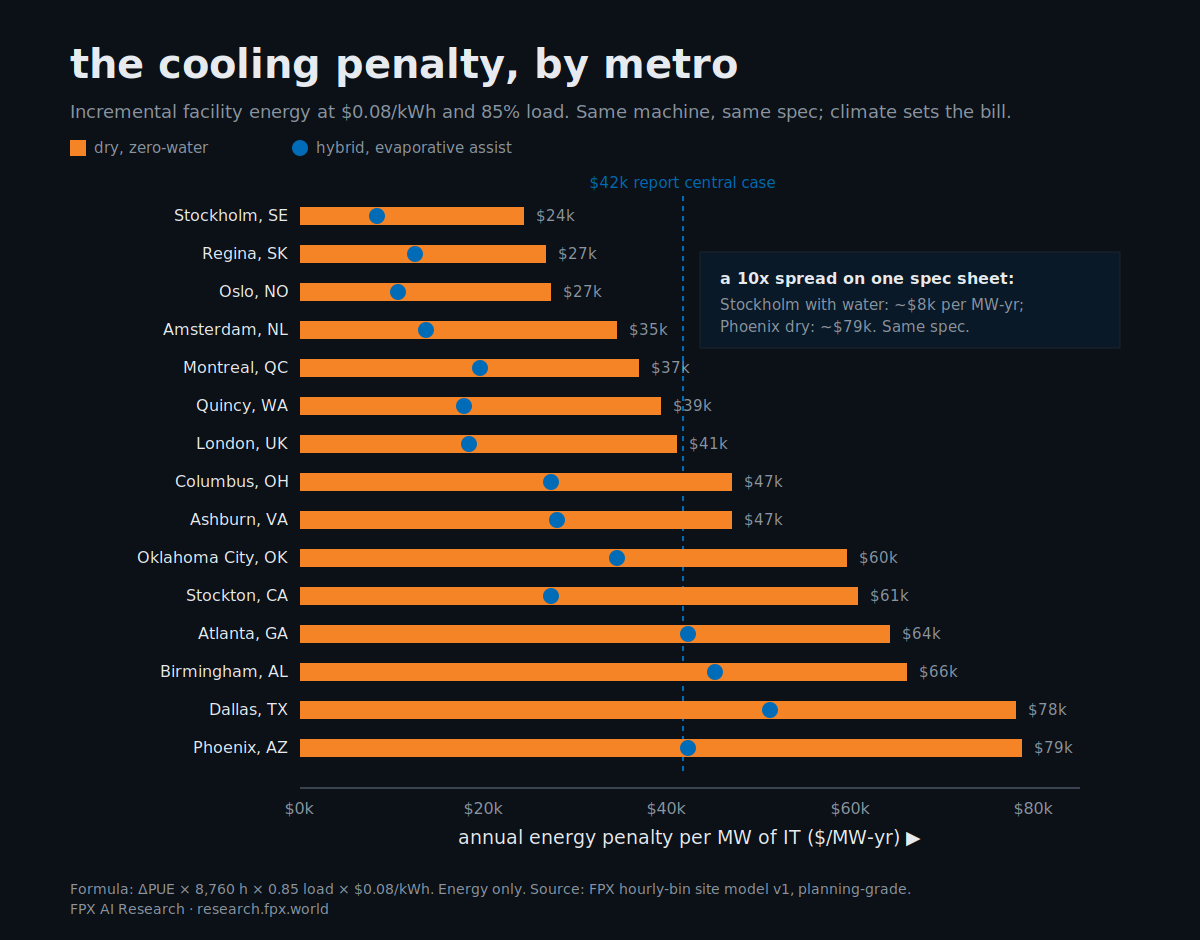

The penalty is real. The easy number was not.

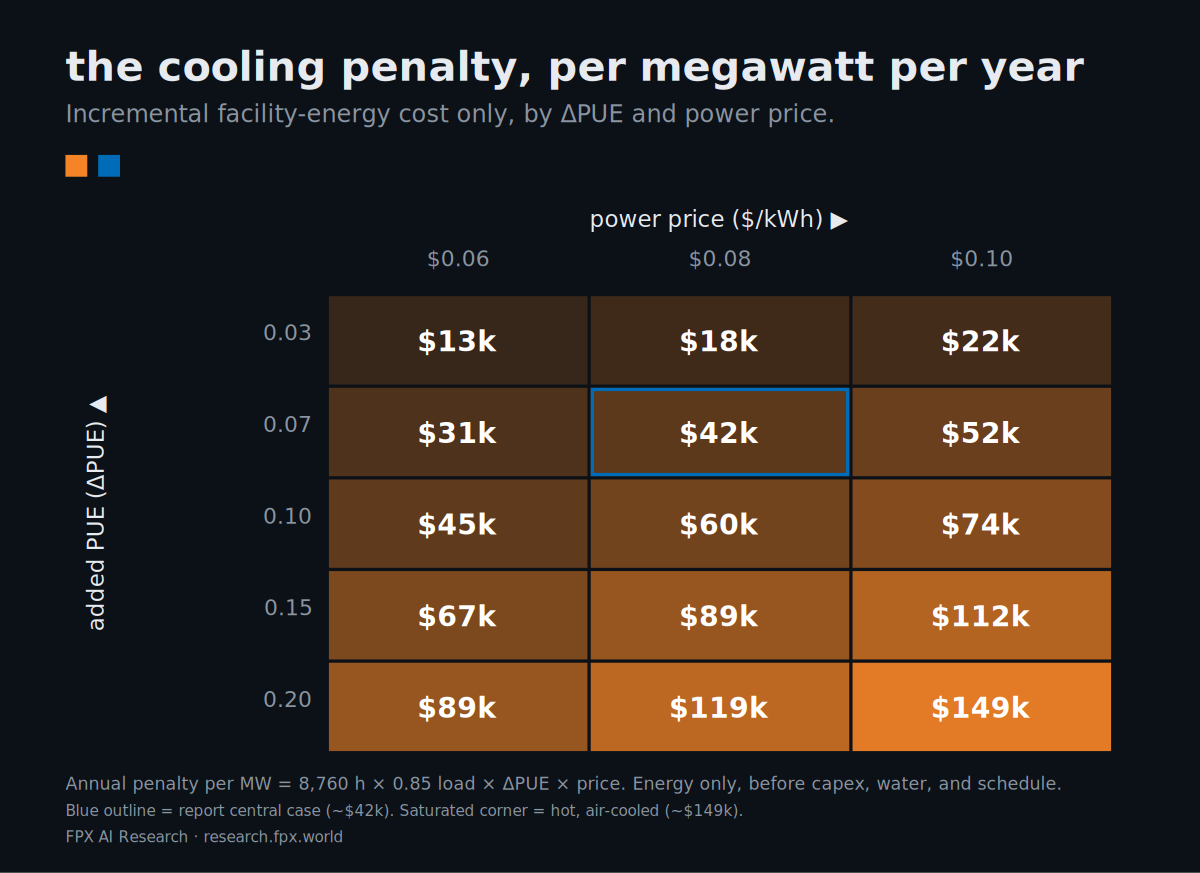

This is the section a private-equity reader will care about most, because it is where the physics turns into a line in a model. It runs on one piece of jargon, so here it is in plain terms. PUE, power usage effectiveness, is how much total electricity a data center burns for every watt that actually reaches the chips. A PUE of 1.0 is a perfect building that exists only on paper; 1.2 means twenty percent overhead for cooling, power conversion, and the rest. The whole cost question reduces to one number: how many extra PUE points does Cerebras’s cooling envelope add over a normal GPU hall, and what does that cost per megawatt.

You cannot derive an annual PUE for a Cerebras hall from a single site’s primary-loop setpoint. You also cannot assume that every Blackwell hall runs at 45°C, or that every CS-3 site runs compressors all year.

The defensible model begins with a delta.

Let the warm-water hall and the CS-3 hall sit in the same market, carry the same IT load, and run at the same utilization. Then estimate how much additional annual PUE the CS-3 design creates after the mechanical engineer models the climate and the plant.

The electricity penalty is:

Annual energy penalty per MW of IT = 8,760 hours × load factor × ΔPUE × power price

At an 85% load factor, each megawatt of IT consumes 7.446 GWh per year before facility overhead.

Here is the resulting sensitivity:

These are FPX scenarios, not measured Cerebras results.

A strong cool-climate plant with water-side economization could land near the low end. A hot, dry site using air-cooled chillers could land near the high end. A design that can reject heat through outside air for most of the year may show only a modest delta despite having chillers in the plant.

The correct central case is therefore not “CS-3 PUE equals 1.30.” It is whatever the hourly-bin model produces for that site.

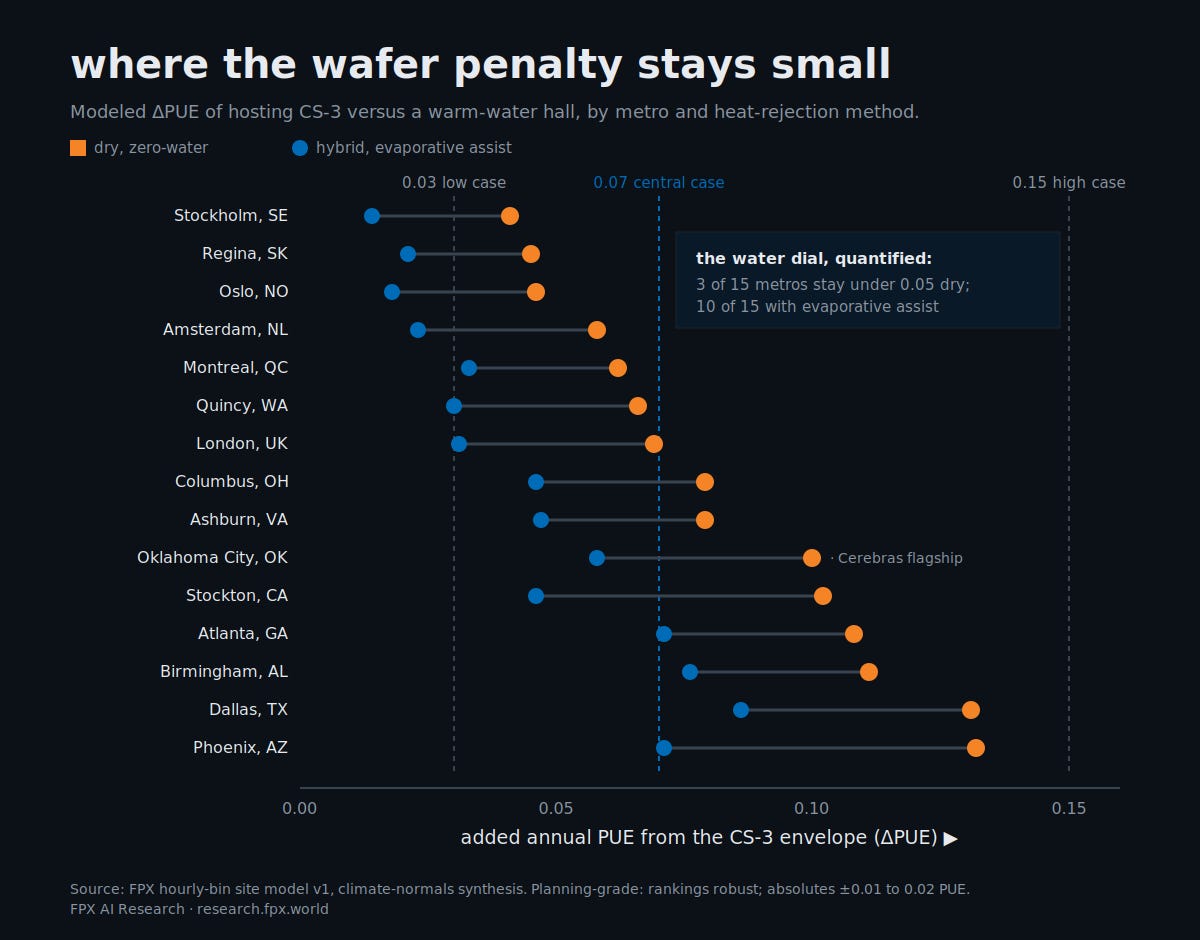

We built a first version of that model (reach out for more info). It synthesizes hourly temperatures from 1991 to 2020 climate normals for fifteen metros, runs the CS-3 chain at a 20°C tenant supply against a 45°C warm-water baseline, and produces a planning-grade ΔPUE per market in two flavors: dry heat rejection that consumes no water, and hybrid evaporative assist that does. The results bracket the table above cleanly. Cool metros like Stockholm, Regina, and Oslo land at 0.04 to 0.05 dry and as low as 0.014 with water. Oklahoma City lands at 0.10 dry and 0.058 hybrid, straddling the 0.07 central case and consistent with Cerebras’s own claim that the site runs on outside air except on the hottest days. Dallas and Phoenix land near 0.13 dry, inside the 0.15 high case, because in extreme heat the warm-water baseline is running chillers too. And the water dial gets a number: only three of the fifteen metros stay under a 0.05 delta with zero-water cooling, while ten do once evaporative assist is allowed. The model is planning-grade, built on climate-normals synthesis rather than measured hourly weather, so absolute values carry roughly ±0.01 to 0.02 of uncertainty while cross-metro rankings are robust. The full market table publishes after a re-run on TMY3 hourly weather files.

For planning, a 0.07 PUE delta at $0.08/kWh produces about $42,000 per MW-year. Treating the contract megawatts as IT load for this sensitivity, the 750 MW committed run-rate would be roughly $31 million a year. At a 0.15 delta, it would be roughly $67 million a year. If the optional capacity takes the relationship to 2 GW, those figures would become about $83 million and $179 million respectively.

That is the energy line only.

The more important penalty may sit above it.

The all-in number has five lines

A real wafer-ready $/MW model needs:

Incremental facility energy.

Water and water-treatment cost, where evaporative rejection is used.

Annualized conversion capex for plant, CDUs, pumps, piping, controls, and electrical support.

Incremental operations and maintenance.

The economic cost of delay, stranded capacity, or a site that cannot pass commissioning.

Only the first line can be estimated cleanly from public information today.

There are no public, comparable bids showing the conversion cost from a Blackwell-ready warm-water hall to a CS-3-qualified hall. Inventing a $/MW retrofit number would make the essay look complete and the model less true.

The honest conclusion is that the compatibility and schedule premium may be larger than the annual electricity premium. A $40,000-per-MW energy delta is survivable. Missing a 250 MW year-end delivery because the cooling loop cannot be commissioned is a different class of problem.

The water-versus-power dial

Water is also conditional, not automatic.

A closed liquid loop does not mean zero site water if heat is ultimately rejected through cooling towers. It can mean close to zero operational water if the plant rejects heat dry or through a system like Nautilus’s natural-water heat exchanger. Oklahoma City says it minimizes water and relies on outside air except on the hottest days. Nautilus says its Stockton design eliminates chillers and cooling towers and consumes no water in the cooling process.

For scale, treating the contracted capacity as IT load, 750 MW at 85% utilization represents about 5.6 billion kWh of annual IT energy. A site-wide WUE of 1.0 L/kWh would therefore imply about 5.6 billion liters of direct annual water use; 2.0 L/kWh would imply about 11.2 billion liters.

That is a sensitivity, not an estimate of Cerebras’s fleet. It becomes relevant only after the heat-rejection method and actual site WUE are known.

The practical conclusion is simple. The CS-3 envelope can force an operator to trade power, water, capex, and economizer hours against one another. Warm-water systems give the designer more room to make that trade. CS-3 gives less.

Question Two: Where Can You Actually Rack a CS-3?

“Liquid-cooled” is not a compatibility standard.

A hall can be ready for direct-to-chip GPU racks and still fail a CS-3 deployment on temperature, normalized flow, chemistry, fittings, residual air load, or controls.

Here is the building’s shopping list, straight from the spec, and most of it reads like plumbing trivia. That is the point. Each line is a way a perfectly good GPU hall can turn out to be wrong for this machine.

20 ± 2°C supply water at the system.

100 LPM per system, or 200 LPM for a two-system rack.

PG25 coolant chemistry and 50-micron filtration.

1.5-inch sanitary fittings and two pairs of supply-and-return connections per rack.

50.4 kW of liquid load and 3.6 kW of air load per rack.

A fully loaded WSE cabinet weighing up to 843 kg.

That is the tenant-side spec. The building still has to answer harder questions.

What temperature can the facility deliver at the tenant demarcation during the worst design day.

How much continuous flow can the headers and CDUs deliver per megawatt at the required differential pressure.

How many economizer hours remain after heat-exchanger approach temperatures are included.

Can the plant support PG25 without compromising other tenants.

Can the residual air system carry the components that are not on liquid.

Can the controls, leak detection, filtration, water treatment, and commissioning process satisfy Cerebras and the customer SLA.

Those questions sort inventory into three piles.

Ready now

Purpose-fitted Cerebras sites and facilities already qualified for the system. Oklahoma City is the clearest public example. Stockton is another, using a very different heat-rejection design. AWS will create a third category inside its own estate.

Convertible with work

Older enterprise data centers with chilled-water plants, mechanical rooms, available pumping head, and enough electrical service can be attractive. They may have lower headline rack density than a new AI hall but better mechanical bones for this exact tenant.

This is the mispricing opportunity.

The GPU market can look at an older chilled-water campus and see obsolete air-cooled enterprise space. Cerebras can look at the same campus and see a plant, a loop, a utility interconnection, and months saved.

Not worth converting

A new warm-water hall built around dry coolers, low-flow CDUs, and no compressor plant may be technically convertible. That does not make it economically sensible.

Adding a parallel cold loop, resizing distribution, and rebuilding controls can strand the design advantage the operator paid for in the first place. In some halls, the right answer will be no.

This is why “GB200-ready” and “CS-3-ready” should be separate fields in a marketplace database.

The CS-3 rack itself is not unusually dense. Its temperature-and-flow signature is unusual. That signature, not the words “liquid cooling,” determines readiness.

Question Three: Where Does 750 MW Land, and Who Collects the Rent?

The OpenAI agreement turns Cerebras into a generator of specialized colocation demand.

The filed contract contemplates Cerebras-, OpenAI-, and subcontractor-controlled data centers. Cerebras remains responsible for the subcontractors it hires, while OpenAI pays the agreed pass-through expenses.

That makes the landlord question central.

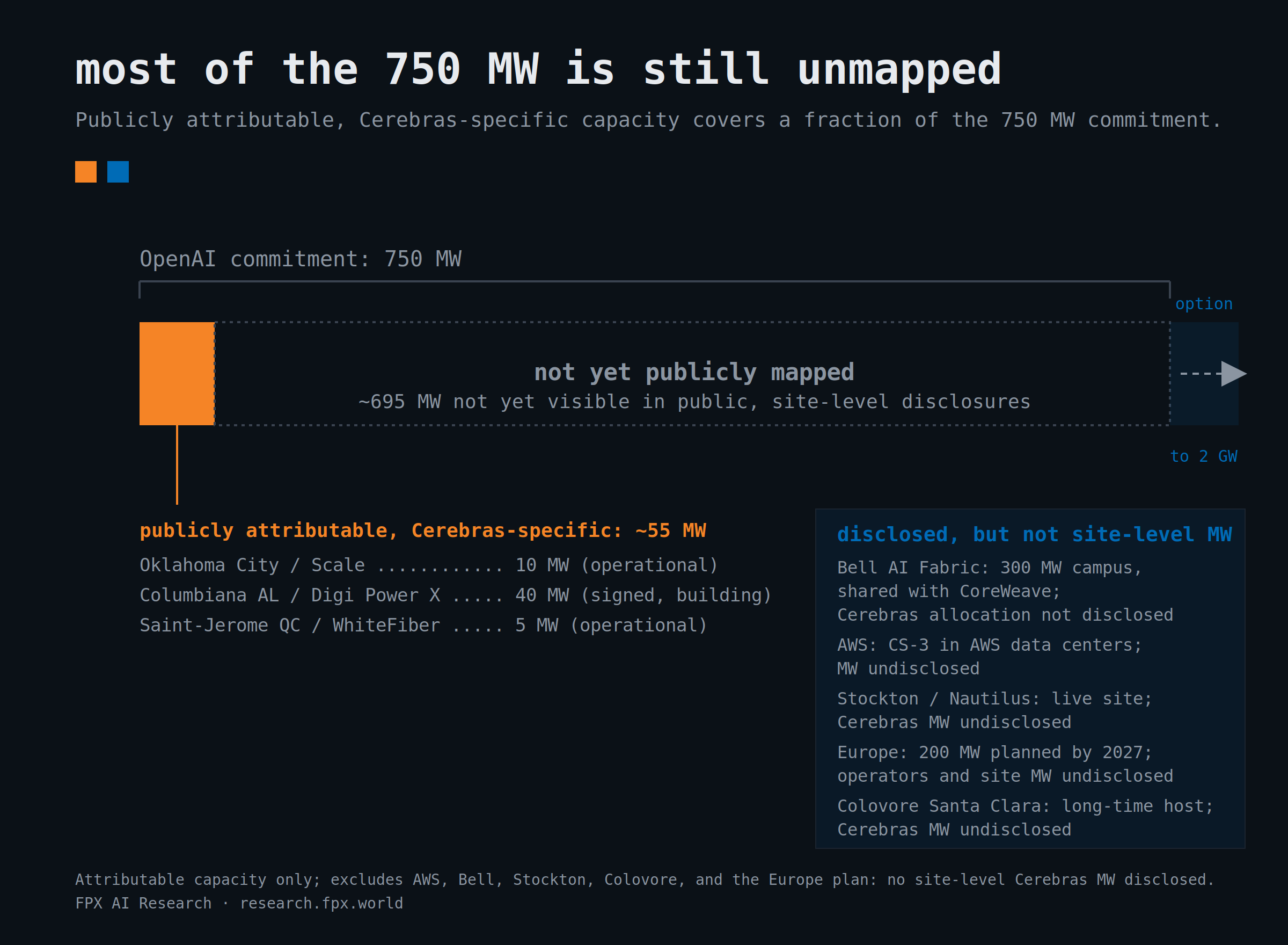

Several pieces are already public:

Oklahoma City / Scale Datacenters: a 10 MW operational facility with more than 300 CS-3 systems reported at the site.

Columbiana, Alabama / Digi Power X: a signed agreement for approximately 40 MW, with a ten-year initial term and a disclosed initial contract value of about $1.1 billion, subject to Digi Power X meeting its obligations.

Saint-Jérôme, Québec / Enovum / WhiteFiber: a 5 MW IT colocation agreement at MTL-3. WhiteFiber’s third-quarter 2025 filing states that installation of the wafer-scale systems was completed in October 2025 and the site is fully operational and generating revenue, and its full-year results credit the Cerebras agreement for the colocation ramp.

Stockton, California / Nautilus: a 2.5 MW agreement announced in 2023, hosted in a facility that advertises 55 kW racks, 1.15 PUE, and no cooling-water consumption.

Santa Clara, California / Colovore: Cerebras’s long-standing Bay Area host, where its Andromeda cluster has run since 2022; a July 2026 UBS note still lists Colovore among the company’s contracted capacity. Cerebras-specific megawatts have never been disclosed.

Saskatchewan / Bell AI Fabric: Bell has announced a 300 MW campus outside Regina, with the first stage expected in the first half of 2027. Bell named Cerebras and CoreWeave as tenants, but the public announcements reviewed here do not disclose how the 300 MW is divided between them.

AWS: CS-3 systems are planned for AWS data centers, but the parties have not publicly disclosed the megawatts or sites.

Europe / operators undisclosed: on July 9, Cerebras announced plans for 200 MW of European capacity by the end of 2027, with first capacity online by the end of 2026 and data centers slated for France, Norway, and Finland; a portion is expected to support OpenAI workloads. No operators or site-level megawatts have been disclosed, so it enters this map as demand, not as attributable capacity.

That list proves the demand is becoming real. It also proves how much remains unmapped.

The named, attributable megawatts do not yet reconcile cleanly to the 750 MW commitment. Put numbers on it. Publicly attributable, Cerebras-specific capacity totals roughly 55 MW: 10 operating in Oklahoma City, about 40 signed in Alabama, and 5 operating in Québec, with Stockton and Colovore live at undisclosed sizes, Bell’s share unstated, and AWS unsized. Against the first 250 MW tranche due at the end of this year, now under six months out, the named capacity covers barely more than a fifth, and the capacity actually operating today, Oklahoma City plus Saint-Jérôme, covers six percent. For calibration, a July UBS note tallies roughly 410 MW of announced contracted power by assuming an even Bell split and counting the European plan; the distance between that contracted figure and the 55 attributable megawatts here is exactly the site-level disclosure gap this section is about. Some of the named capacity may also serve customers outside the OpenAI agreement. The remaining landing zones are therefore not a footnote. They are the execution thesis.

Cerebras does not dispute the difficulty. On its June earnings call, Feldman described data-center capacity as “at a premium” and the hunt for it as a “dog fight,” while listing early discussions running from Israel to Indonesia. The constraint this report models is the one the company says it is living.